Starfighters Space: A 1950s “Flying Coffin” Masquerading as the Next SpaceX, Led by Vancouver Stock Promotion Network

Published on April 10, 2026

Source: Screenshot of public post by NYSE on LinkedIn. Reproduced for purposes of commentary and criticism of a publicly traded security (17 U.S.C. § 107).

Summary

- Starfighters Space, Inc. (“FJET”; “the Company”) is a zero-revenue vaporware company with antiquated technology and unqualified leadership, masquerading as an emerging launch platform. Our research found no credible rocket program – and substantial evidence the Company exists primarily to enrich its early backers.

- FJET’s key backer, Fortuna, is led by Justus Parmar, who claims he “builds companies that are shaping the future of the American economy.” In reality, Parmar is no more than a Vancouver stock promoter, who has spent two decades riding hot themes – mobility, crypto, cannabis, critical minerals, and now space – leaving a trail of over a dozen collapsed, delisted, or cease-traded companies in his wake.

- Parmar began his career as a Vancouver stockbroker, bringing companies like Reliq Health Technologies (TSXV: RHT) public. Reliq became the subject of a British Columbia Securities Commission (BCSC) investigation into a $46 million alleged pump-and-dump and saw its stock decline over 99% before being cease-traded.

- One of Fortuna’s earliest investments was Atlas Blockchain, an aspiring crypto miner. Atlas was aggressively promoted alongside notorious pump-and-dump operators like Fred Sharp, whom the SEC charged for a $1 billion illegal trading operation labeled “a sophisticated, multiyear, multinational attack on the United States financial markets and United States retail investors.”

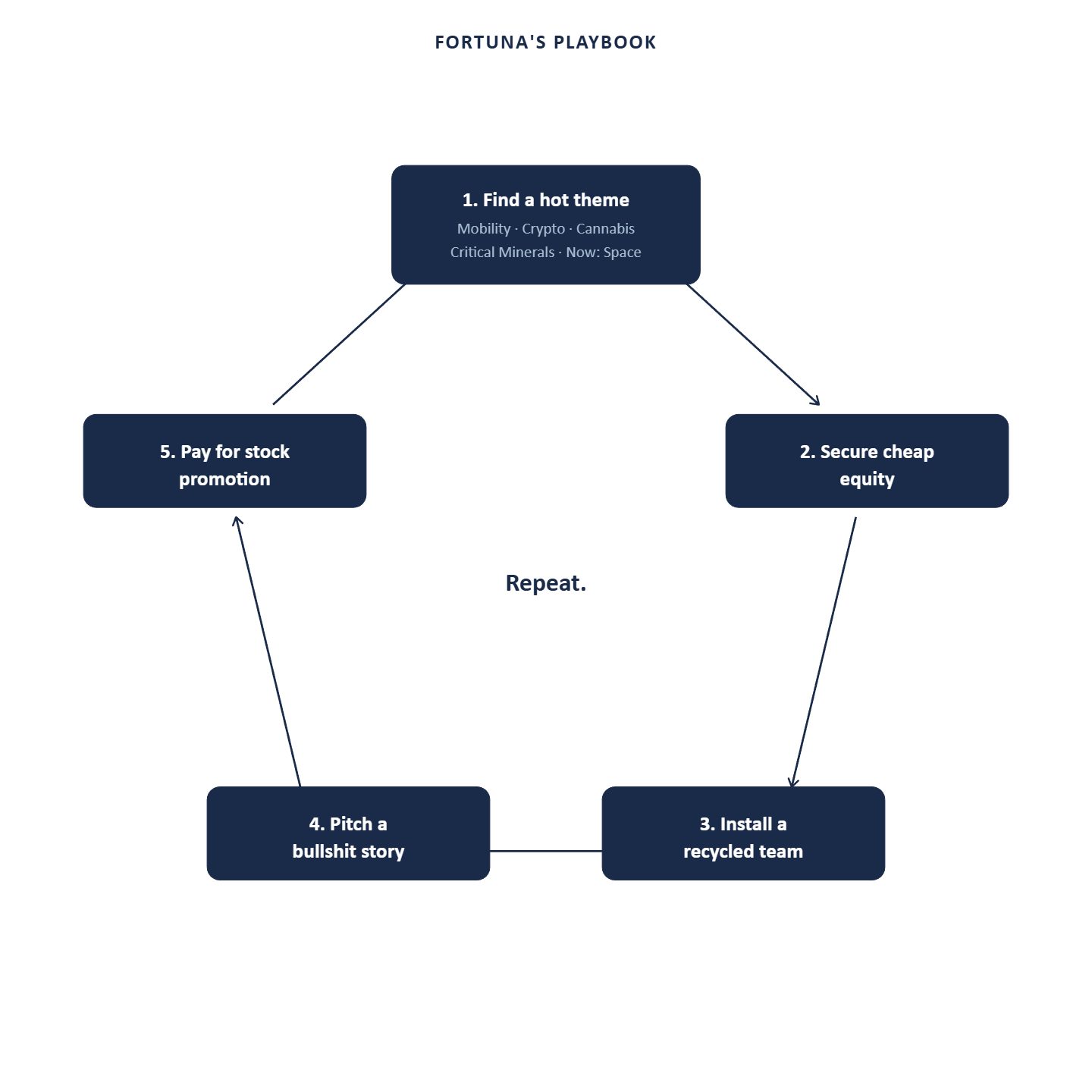

- Fortuna used the same playbook across these collapsed companies: find a hot theme, secure cheap equity, install a recycled team of Vancouver affiliates, pitch a bullshit story, and pay for rampant stock promotion. We observe these events unfolding at FJET in real-time.

- FJET issued penny warrants for 15 million shares with a $0.33 strike – a 91% discount to IPO – just weeks before it signed a consulting agreement with Fortuna in September 2022. A Form 4 from affiliate Sean Bromley, indicates Fortuna’s team received the distribution. Four trading days after the IPO, 11.7 million of the warrants were cashless exercised at a $16.46 VWAP – a potential $192 million payday.

- Fortuna has had six affiliates at FJET, including four directors and two CFOs. They have cycled through dozens of the firm’s companies in varying roles.

- We uncovered relentless and misleading paid promotion for FJET stock’s from CDMG, Inc., whose founder is described as having “a history of promoting scams and deceptive schemes, including fraudulent investment and nutrition products targeting seniors.” Fortuna has engaged CDMG at several other companies. They were given 2.75 million warrants at $0.33, now worth ~$15 million.

- Parmar’s groomsman and lifelong associate, Shane Parhar (“Shane”), has mysteriously been front-and-center at key FJET corporate events. Shane is a registered stockbroker at small Canadian shop, Mackie Research Capital (“Mackie”), and holds no disclosed role with FJET or Fortuna.

- In 2017, Shane was named in a BCSC investigation into securities trading at Mackie where regulators seized his work computer and personal smartphone.

- Shane’s associates include key players of the BridgeMark Financial fraud — Justin Liu, a former Mackie colleague, Anthony Jackson, and Aly Babu Mawji. Both Liu and Jackson faced trading bans in Canadian capital markets and paid millions in fines to regulators. Mawji was imprisoned in Germany for 38 months and banned from Ontario capital markets for a €25.7 million “pump-and-dump scheme”.

- FJET has attempted to air launch rockets from Cold War-era F-104s for over a decade and FAILED. Its first three attempts – a 2011 university collaboration, a 2016 CubeSat startup partnership, and a 2022 Italian research program – all failed to launch a single rocket. Immediately after Fortuna’s engagement FJET began promoting its fourth iteration.

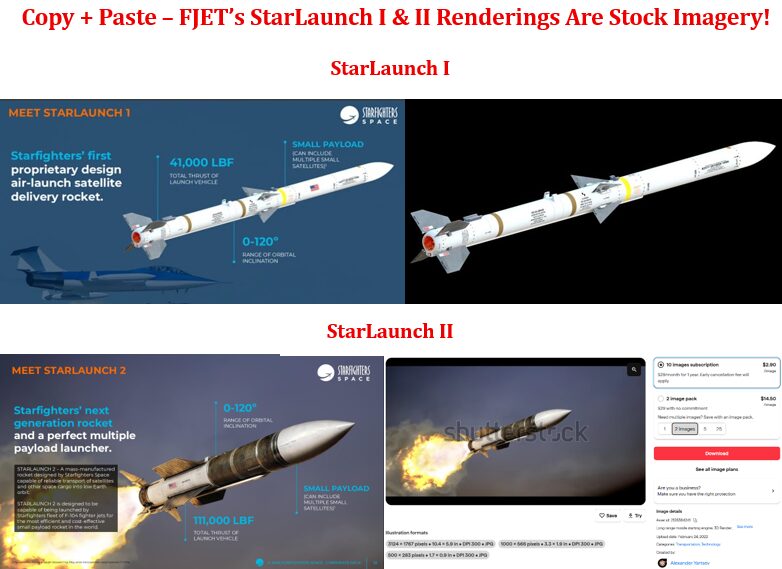

- The rocket renderings FJET has used in investor materials since 2022 are stock art. StarLaunch I is concept art of a commonly used missile – FJET slapped an American flag on it and left the original serial number on the body. StarLaunch II is available for sale at $2.90 per 10-pack to Shutterstock subscribers.

- FJET has missed every development milestone communicated to investors since 2022. It has repeatedly promised launch licensing, as well as commercialization and testing milestones. 2022, 2023, 2024, and 2025. None were delivered.

- We obtained FAA documents which show FJET’s fleet of seven F-104s is not even certified for experimental air-launch. The FAA explicitly states that “air launches of payloads are not authorized.”

- A rocket launch expert we consulted reviewed FJET’s program specs: “If you look at that rocket, that rocket is like a bottle rocket that you could practically do in your backyard.”

- Despite the absence of any sort of rocket program and key metrics, FJET claims it can launch 100kg to Lower Earth Orbit (LEO). We conducted a comprehensive analysis using the Tsiolkovsky rocket equation where we gave FJET extremely generous assumptions – SpaceX level structural efficiency and engine efficiency. Even in this blue-sky scenario, we estimate FJET’s F-104 could deliver 28kg into orbit, ~70% lower than its claimed payload capacity and just ~10% of the next smallest commercial rocket we found (Electron).

- The only commercially successful air launch vehicle in three decades – Pegasus – required a rocket 22 times heavier than anything FJET’s F-104 can carry, and SpaceX has since made it economically obsolete. Before it, Virgin Orbit spent $1 billion and went bankrupt. Stratolaunch built the world’s largest airplane and abandoned orbital launch entirely. DARPA and Boeing spent $164 million before propellant explosions ended the program. We believe the F-104 will soon be reunited with these other carrier aircraft in the great hangar in the sky.

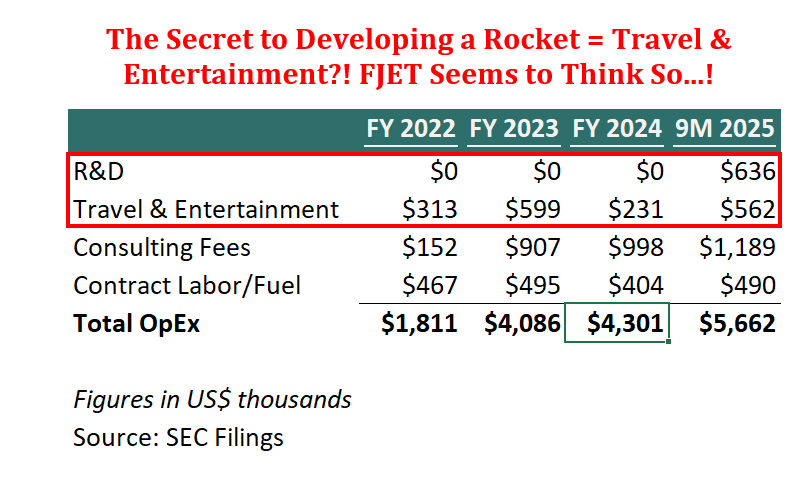

- In Fortuna’s first three years as an advisor to FJET, the Company spent zero dollars on R&D. In the first nine months of 2025 it spent 3x more on consulting fees plus travel and entertainment than R&D. FJET appears to have zero employees. Its CEO has no engineering experience whatsoever, while its CFO came from a bankrupt Canadian film studio.

- Rick Svetkoff, FJET’s founder, CEO, Chairman, and largest shareholder, resigned two months after the IPO. His wife, the Corporate Secretary, went with him. His resignation letter cited “misallocation of corporate resources” and “the assignment of inexperienced personnel to critical positions.”

- Last year FJET’s auditor, Adeptus Partners, was sanctioned by the PCAOB for “violations related to supervision, review, and quality control.” The Company has disclosed material weaknesses in internal controls and failed to timely file its 10-K last month.

- With roughly $25 million in cash at the end of September and $15 million in estimated annual burn, FJET’s runway is short. A launch expert we hired estimated reaching a first orbital attempt would require ~$50 million. FJET has raised a fraction of that – and spent a measly amount of it on rocket development.

Initial Disclosure: Following our research, Umibōzu Research holds a short position in shares of Starfighters Space (NYSE American: FJET). This report reflects our analysis and opinions. We urge readers to conduct their own independent due diligence. A full disclaimer appears at https://umibozuresearch.com/disclaimer/

Part 1: Fortuna – How FJET’s IPO Was Engineered by Some of Vancouver’s Finest Stock Promoters

Justus Parmar Built His Career on Vancouver Penny Stocks Before Taking His Talents to South Miami Beach

Starfighters Space, Inc. (“FJET”; “the Company”) has been shepherded public by Fortuna Investments, a self-described venture capital firm founded in 2015 and led by Justus Parmar. Vying for celebrity investor status, Parmar documents a lavish lifestyle on his Instagram while frequently appearing on Bloomberg and CNBC.

Fortuna claims to have “invested in over 125 startups,” with Parmar purportedly “advising on over $1 billion in transactions” and helping “dozens of companies go public.”

For a firm boasting of a “successful track record across Canada and globally” with twelve investment sectors on its website, the absence of a disclosed portfolio or list of exits is conspicuous. More glaring, despite promoting its commitment to “American ingenuity” and claiming to have four US offices, the firm appears to lack any real operational presence in the country. Its Midland, Texas location is a co-working space. Its Los Angeles office is registered to Parmar’s previous residence. Its New York address is nowhere to be found. And its Miami headquarters – whose launch was the subject of considerable fanfare – was taken over by a paddleboard rental shop.

Our investigator visited 1800 Sunset Harbour in Miami Beach and spoke with the owner of the paddleboard rental shop who had previously leased another unit in the complex. They told us Fortuna had moved out a few months ago and that they’d only ever seen someone at the office once.

A look at the record explains why: behind Parmar’s carefully curated public image and Fortuna’s “America-first” branding lies a long trail of over a dozen failed public listings in Canada spanning e-mobility, crypto, cannabis, critical minerals, and more. Parmar is one of Vancouver’s most under-the-radar yet prolific stock promoters.

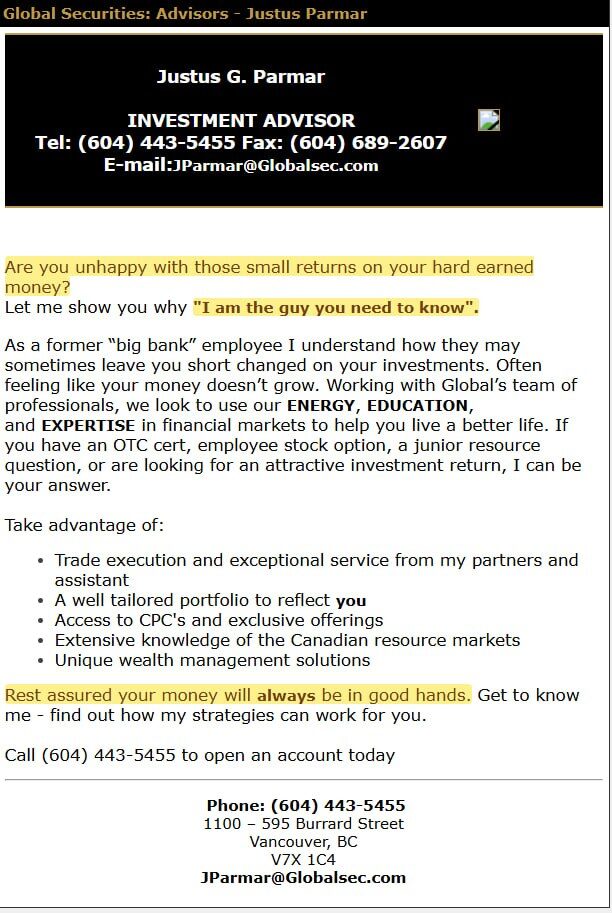

Parmar began his career at Macquarie Group and Global Securities Corp., where his advisor profile telegraphed his early ambition: “Are you unhappy with those small returns on your hard earned money? Let me show you why I’m the guy you need to know.”

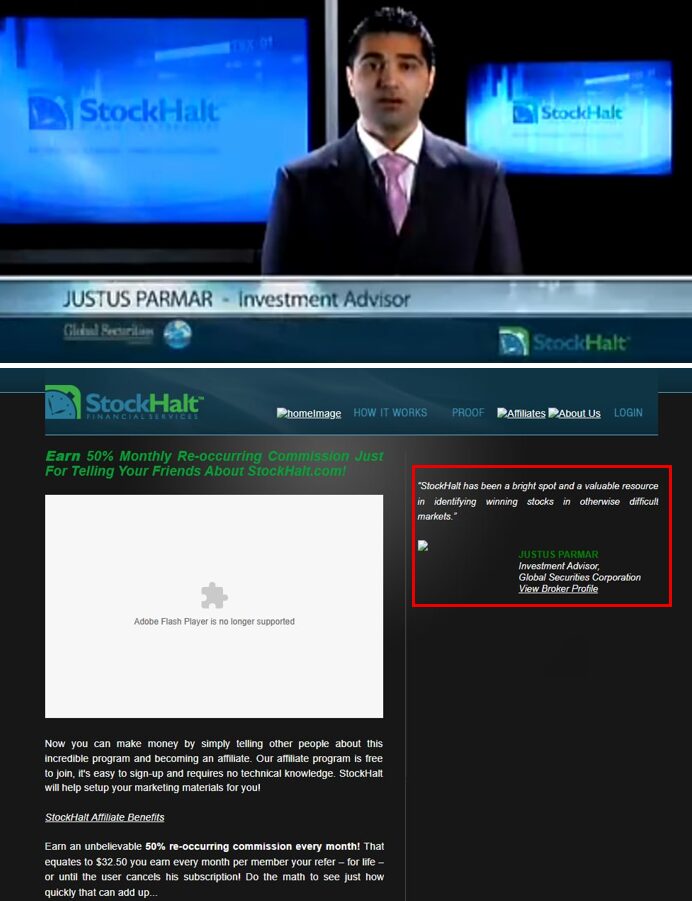

Clips from as early as 2007 show Parmar promoting StockHalt.com, described as “a revolutionary new tool… that instantly delivers news on halted stocks” Aimed at retail investors, StockHalt had an affiliate marketing program that promised “50% recurring commission every month.”

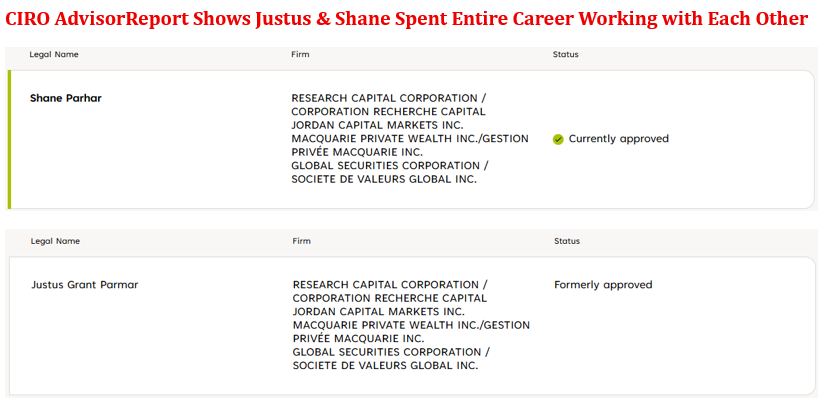

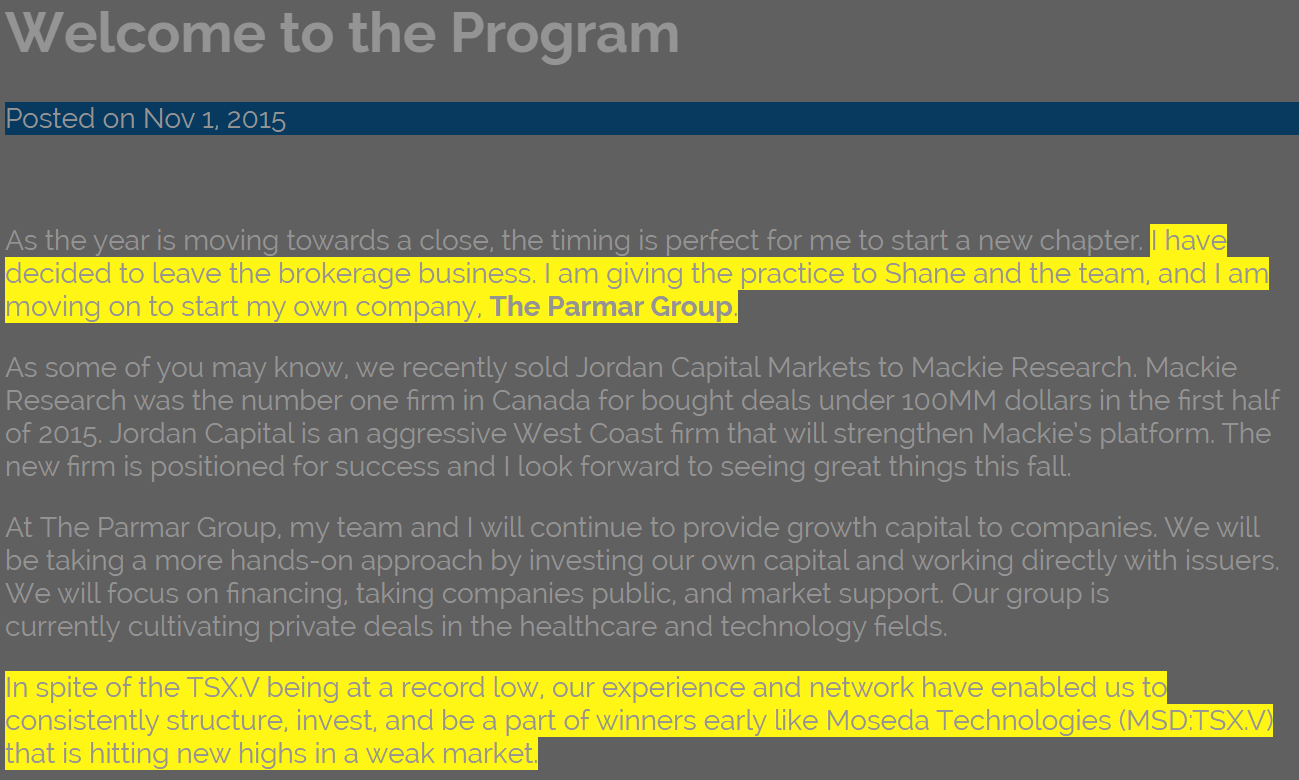

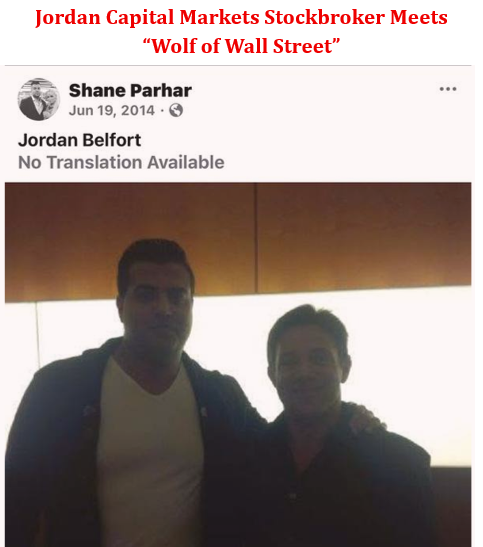

Parmar later joined Jordan Capital Markets, a Vancouver broker-dealer focused on Canadian microcaps, where he worked alongside Shane Parhar (“Shane”), a key partner throughout his career, starring in the FJET story today. The two worked together at Macquarie, then Global Securities, and then Jordan Capital. When Parmar left in November 2015 to launch his own shop, he handed Shane his book of business.

Jordan Capital banked numerous Canadian microcaps under Parmar and Shane. Among their co-led deals was Moseda Technologies (aka Reliq Health Technologies), a healthcare technology startup. Parmar touted his network enabling them to “consistently structure, invest, and be a part of winners early like Moseda Technologies.”

As just one documented collapse, Moseda/Reliq became the subject of a British Columbia Securities Commission (BCSC) investigation into a $46 million alleged pump-and-dump scheme and saw its stock decline over 99% before being cease-traded.

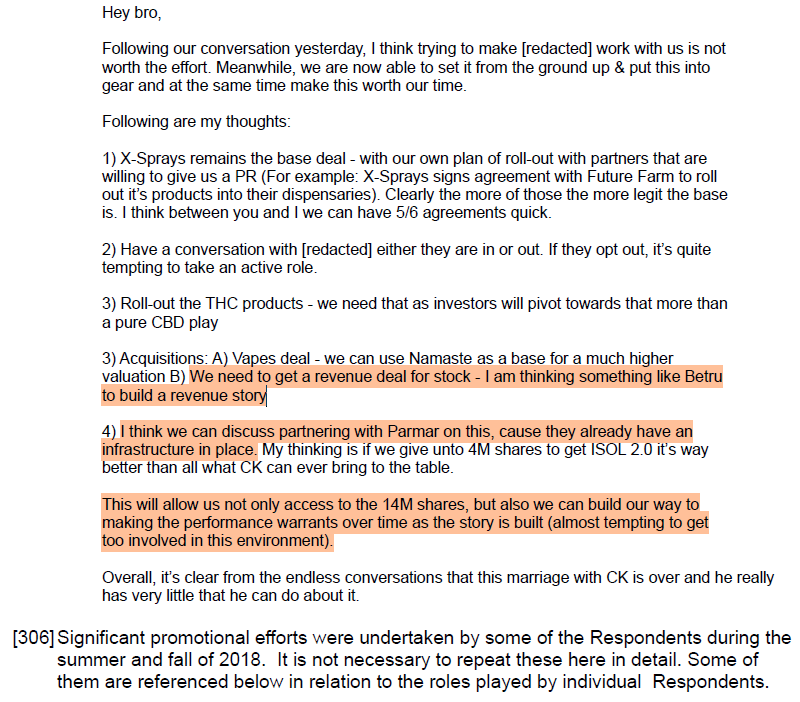

Documents from the investigation revealed conversations between Moseda/Reliq insiders about partnering with “Parmar… cause they already have an infrastructure in place” in reference to a promotional campaign where they planned to “get a revenue deal for [the] stock” and “build a revenue story” that would unlock vesting warrants in the company.

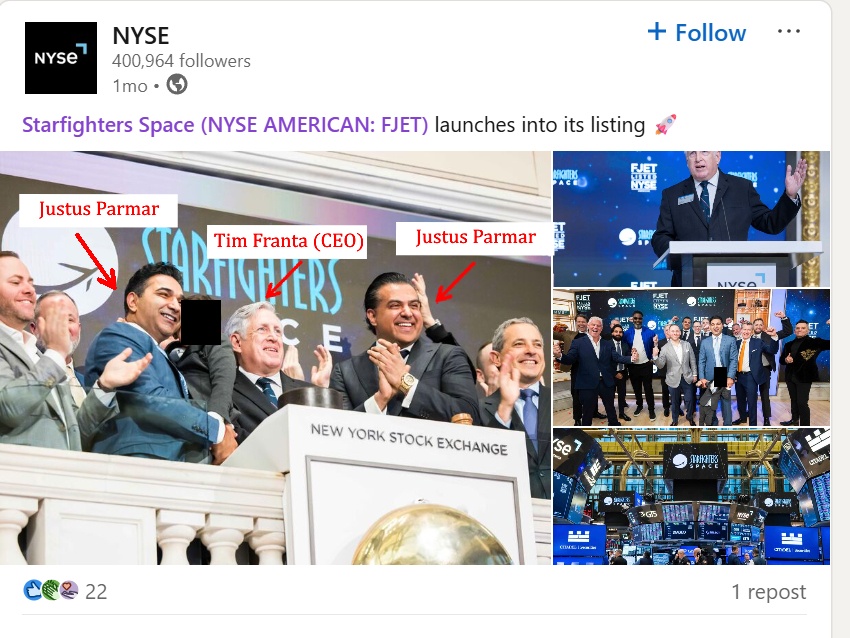

Fast forward to the present. Shane – still a registered advisor at Mackie Research Capital (“Mackie”) – holds no disclosed role at FJET or Fortuna yet appears to have been central to the Company’s IPO. He can be seen wearing FJET gear when Mike Pompeo visited the Kennedy Space Center in December 2023 and was front and center at FJET’s NYSE bell-ringing earlier this year – an event the Company’s own founder and largest shareholder did not appear to attend.

Source: Screenshot of public post by NYSE on LinkedIn. Reproduced for purposes of commentary and criticism of a publicly traded security (17 U.S.C. § 107).

Shane’s associate at Mackie, Ravinder “Roger” Singh Jouhal, who refers to Parmar as a “brother and mentor”, was also in attendance at the event and can be seen sporting FJET merch on Instagram following the IPO. He called it “years of work”. Jouhal maintains an operational presence in Midland, Texas – the same city where Fortuna recently opened an office and where FJET has a deal with the Midland Development Corporation.

The presence of Shane and his affiliates at FJET is notable given his background. Shane was one of four individuals named in a 2017 BCSC investigation into securities trading at Mackie, with regulators seizing his work computer and personal smartphone. He obtained a stay blocking BCSC staff from reviewing the seized materials.

In 2018, Shane was pictured at a yacht party celebrating the birthday of Justin Liu – a former colleague from Mackie – alongside Anthony Jackson and Aly Babu Mawji. Liu and Jackson were the two “primary architects” behind the illegal BridgeMark Financial operation. In the infamous consulting scheme Liu’s affiliated companies agreed to a ten-year trading ban and paid a $950,000 fine to the BCSC. Jackson was hit with a $1.75 million class action settlement, $100,000 in BCSC fines, a suite of temporary capital markets sanctions, and an eight-year ban from serving as a public company director. Meanwhile, Mawji, a “convicted fraudster”, was sentenced to 38 months in prison in Germany and banned from Ontario capital markets for “carrying out a pump-and-dump scheme” where he “defrauded €25.7 million from investors.” Following his imprisonment in Germany, Mawji was also involved in the BridgeMark Group scheme as well.

PennystockMaxxing: Fortuna’s Stock Promotion Playbook

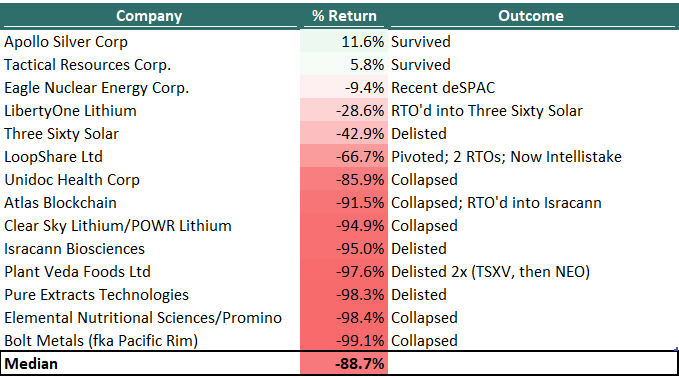

FJET may be Fortuna’s first foray into US markets, but the scheme is not new. We reviewed companies where Fortuna had installed its team and the outcome is remarkably consistent. The underlying businesses almost uniformly fail. The stocks collapse and become cease-traded or delisted.

We uncovered the multi-stage playbook Fortuna has used to promote stocks.

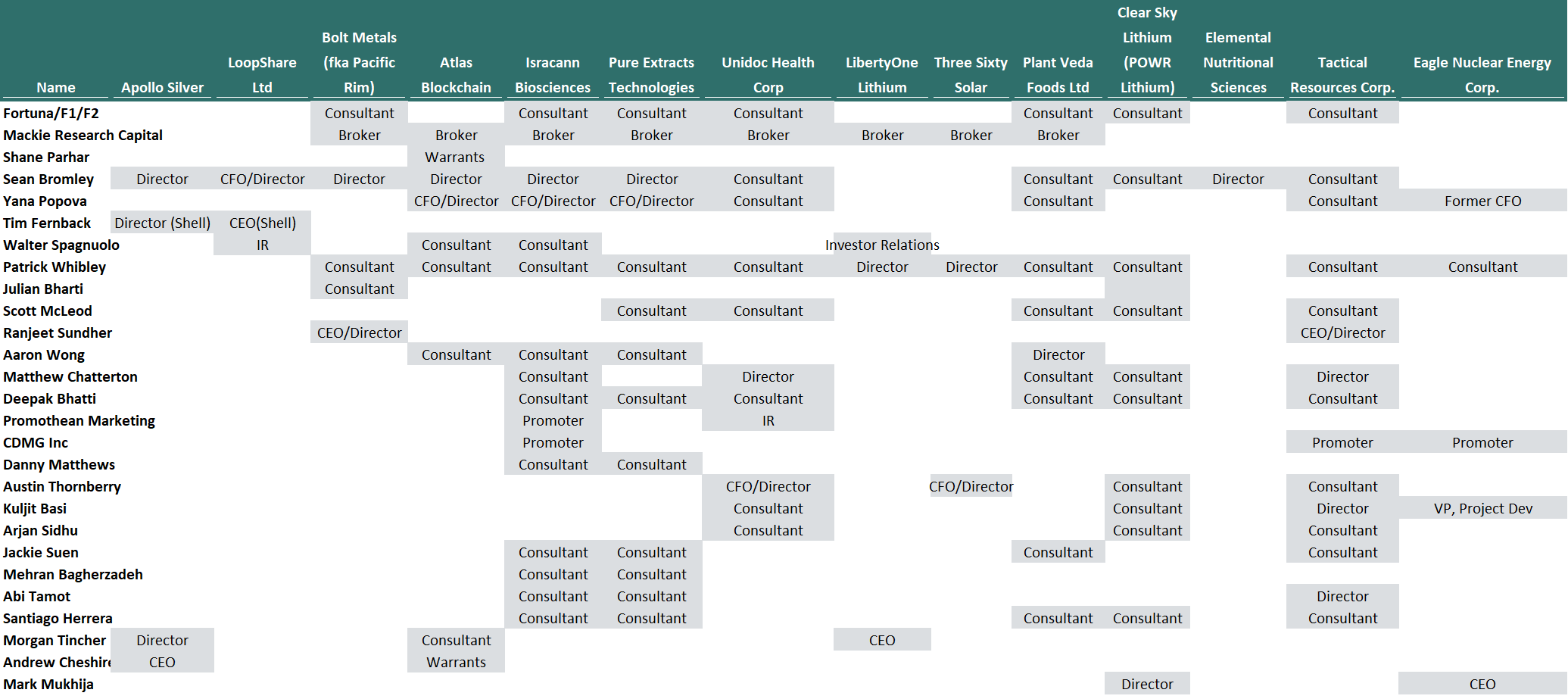

Across Fortuna’s failures, the same cluster of individuals – cycling through executive, director, and consultant roles – appears in filings. The names change positions and the themes change, but the network and outcomes are consistent.

While we suspect the network runs even deeper and wider, the names, entities, and companies we found from hours and hours of sifting through Stone Age SEDAR filings show that 27 individuals/entities filled 113 roles across 14 Fortuna companies, an average of four companies per person. Two individuals – Sean Bromley and Patrick Whibley – each appear in 11 companies.

People/Entities: (1) Sean Bromley (2) Patrick Whibley (3) Yana Popova (4) Deepak Bhatti (5) Scott McLeod (6) Matthew Chatterton (7) Santiago Herrera (8) Walter Spagnuolo (9) Aaron Wong (10) Austin Thornberry (11) Kuljit Basi (12) Jackie Suen (13) Arjan Sidhu (14) Abi Tamot (15) Morgan Tincher (16) Tim Fernback (17) Ranjeet Sundher (18) Danny Matthews (19) Mehran Bagherzadeh (20) Andrew Cheshire (21) Mark Mukhija (22) Shane Parhar (23) Julian Bharti (24) Promothean Marketing (25) CDMG Inc (26) Mackie Research Capital (27) Fortuna/F1/F2

Companies: (1) Apollo Silver (2) LoopShare Ltd (3) Bolt Metals fka Pacific Rim (4) Atlas Blockchain (5) Isracann Biosciences (6) Pure Extracts Technologies (7) Unidoc Health Corp (8) LibertyOne Lithium (9) Three Sixty Solar (10) Plant Veda Foods Ltd (11) Clear Sky Lithium/POWR Lithium (12) Elemental Nutritional Sciences (13) Tactical Resources Corp. (14) Eagle Nuclear Energy Corp.

Case Study #1 – LOOPShare: Parmar’s “Big Deal” in E-Mobility That Generated Less Than $1 Million in Revenue Before Pivoting to Ray J’s E-Bike Brand

LOOPShare, Ltd. (TSXV: LOOP) (“Loop”) was a scooter-sharing platform which came public through a reverse merger between Saturna Green Systems and Kenna Resources, a TSXV-listed mining shell, whose CFO, Anthony Jackson, would later become the central figure in the BridgeMark Financial fraud.

The deal came just as venture capital was allocating heavily to rideshare and e-mobility companies like Uber and Lyft. A retail investor journal caught wave of Parmar’s involvement describing Loop as “right in the middle of the ‘sharing economy’ movement”:

“Parmar’s big deal right now is a scooter rental outfit named Loop. You may have seen it featured in the news because it’s doing business now. It’s not a notion, not a plan, not a ‘coming soon’, it’s real, they’re opening operations and selling franchise agreements, and its potential market is insane.”

A November 2015 archive of Fortuna’s website lists Kenna as one of its “investments”. In December 2015, Kenna issued 3.2 million units at $0.115 and warrants at $0.25 in a deal led by Mackie. While undisclosed, we suspect that Fortuna participated in the raise as Sean Bromley was appointed to the board concurrently.

In June 2016, Kenna and Saturna completed their reverse merger. Having been engaged to find a transaction by both parties, Fortuna was issued 2.9 million shares at a deemed price of $0.20.

Loop targeted a presence in 11 cities. In its initial months as a public company it presented progress on that plan, announcing field trials in Miami, Vancouver, and Beirut. Specifically for its 2017 fiscal year, the company planned a deployment of 110 scooters in Vancouver. In Beirut, the company planned to be the first commercial operator of electric scooters. It initially deployed 15 scooters, targeting a full scale roll-out of 70 in 2017.

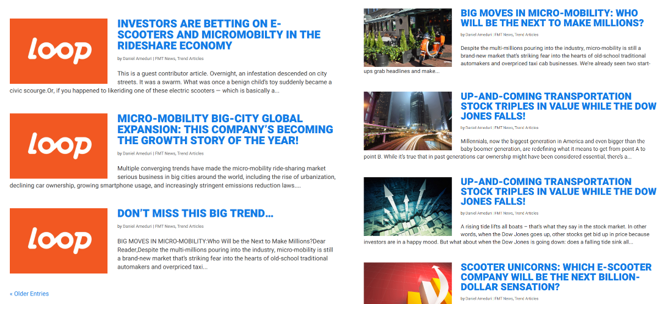

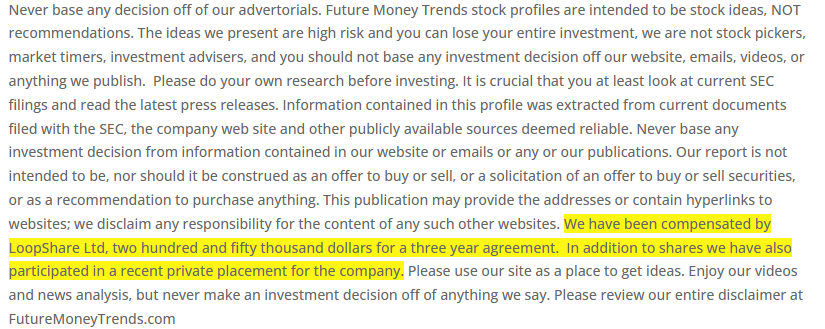

As investors anticipated the multi-city launch, Loop’s stock was being heavily promoted by Future Money Trends, LLC. and Dolce Vita IR. Paid articles from these outlets hyped up the opportunity. One article urged investors, “Now’s a great time to start looking for the next micro-mobility superstar, and I believe it’s going to be LoopShare”, adding “Don’t miss this big trend…”.

Despite the hype, this commercial roll-out never materialized. After failing to hit its targets for Beirut in 2017, the company targeted an even larger fleet in 2018 of 165 scooters. By mid 2018, Loop had deployed just 22 scooters in Beirut. In Miami, the scooters were never rolled out at all. At its peak, Loop generated less than $1 million in annual revenue. The bulk of that revenue traced back to a circular related-party arrangement in which Loop used funds it had been advanced to purchase software from an entity owned by its founder. For context, legitimate e-mobility companies like Bird and Lime deployed hundreds of thousands of scooters across the globe.

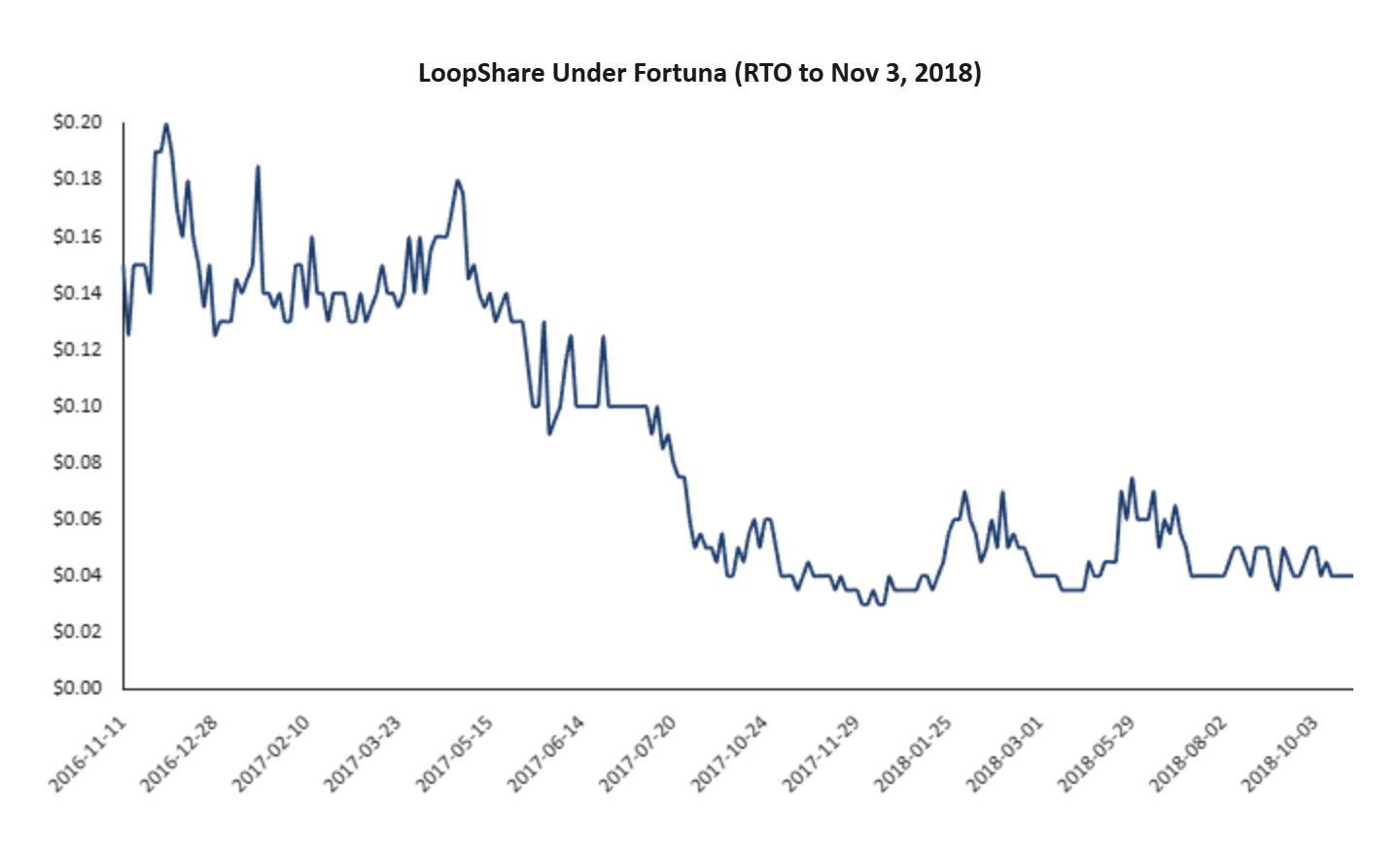

Loop’s stock traded down to $0.05 per share as Fortuna’s Bromley departed the company in November 2018. Ironically, the same Stockhouse article that had promoted Loop as Parmar’s “next big deal” specifically expressed contempt for IPOs where “all the opening paper gets dumped for the next big thing and [the stock] drops to $0.05 for the next three years.”

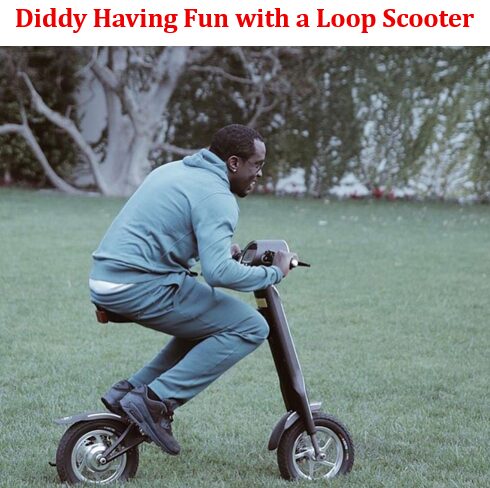

With its scooter-sharing ambitions in tatters and the stock in freefall, Loop went on to acquire an e-scooter/e-bike brand owned by R&B singer, Ray J. The “Scoot-E-Bike” was endorsed by celebrities like Diddy and Steph Curry, despite lacking safety certifications. The scooter product business failed too.

Loop failed to file its financials throughout COVID-19 before ultimately pivoting from mobility to gluten-free food. In November 2021 it merged with VGAN Brands, Inc. and changed its name to The Good Flour Corp. (TSXV: GFCO) (“Good Flour”). As the ensuing case studies show, Loop was just the beta-launch of Fortuna’s playbook.

Case Study 2A – Atlas Blockchain: Minimum Hash Rate, Maximum Promote Rate

Atlas Cloud Enterprises (CSE: AKE) (“Atlas”) was a left-for-dead, IT equipment company with less than $200K in annual revenue. After the Fortuna network arrived, it changed its name to Atlas Blockchain Group and began promoting a plan to become “the lowest cost producer in the blockchain and digital currency mining sector.”

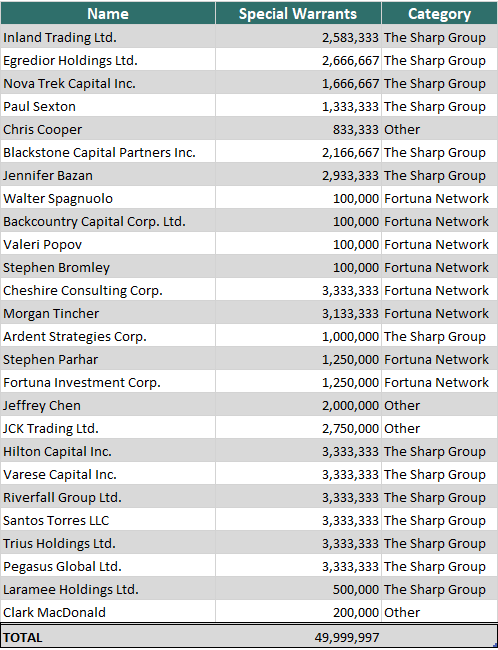

In late October 2017, Atlas raised $3 million from the sale of 50 million Special Warrants each consisting of a warrant and common share. The Special Warrants were issued to Fortuna and other investors at more than a 75% discount to a subsequent private placement led by Mackie just two months later. In that placement, Atlas issued ~39.5 million units, raising ~$13.8 million, with proceeds earmarked to the purchase of electricity facilities and R&D for secure blockchain storage. Atlas had seemingly shed its image as a dying IT business and become a blockchain innovator overnight.

The Special Warrants were registered for resale in the weeks following the private placement. Filings reveal that the distribution went substantially to Fortuna’s network and a who’s who of Vancouver pump-and-dumps.

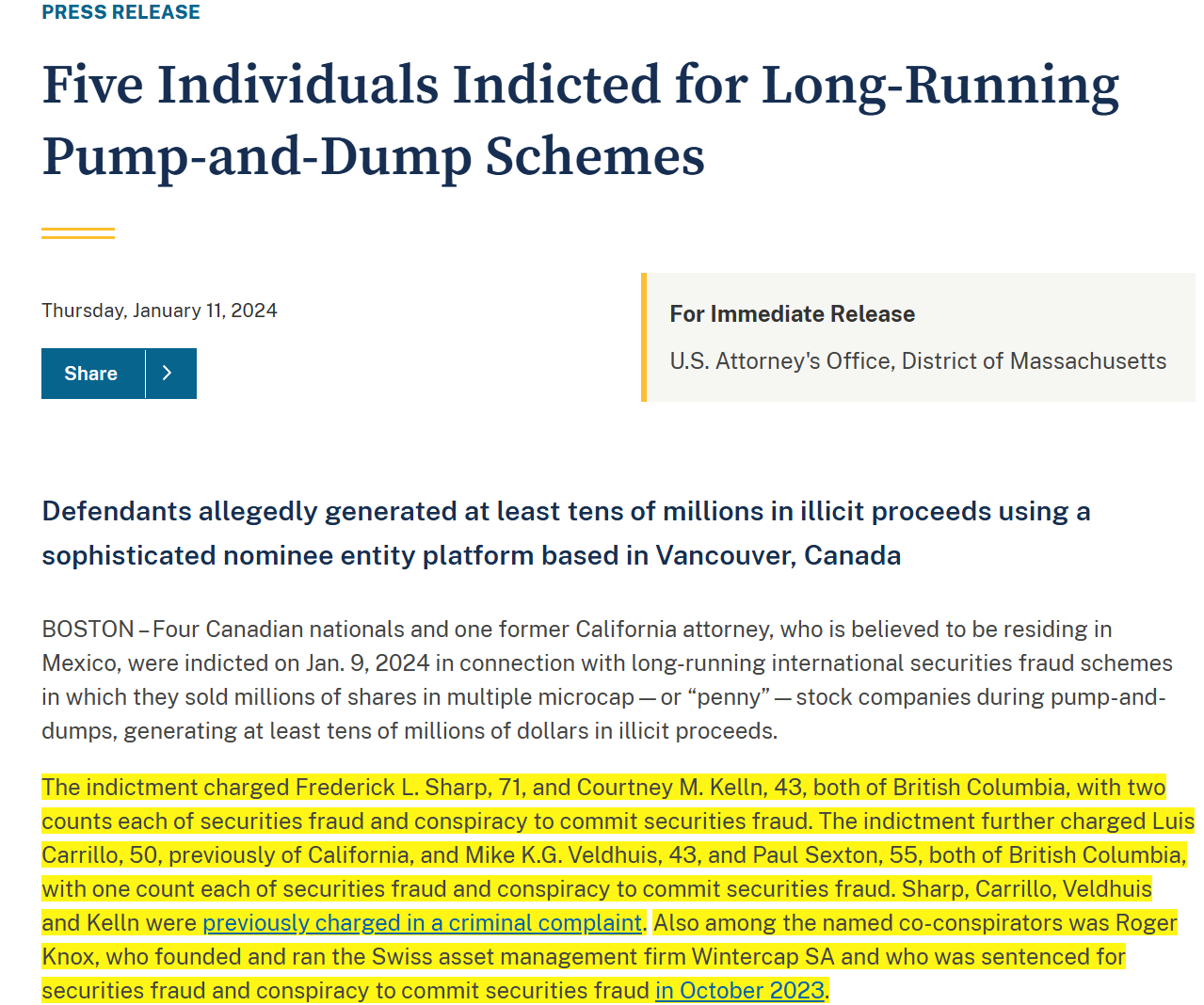

The finder/agent on the deal was Morris Capital Inc., a Belize-registered entity identified by Quebec’s securities regulator as part of the offshore architecture used by Fred Sharp, whom the SEC called the “mastermind” of a “sophisticated, multiyear, multinational attack on the United States financial markets” generating over $1 billion in illegal trading proceeds across hundreds of penny stock companies. A US federal judge ordered Sharp to pay $52.9 million in disgorgement and penalties; the BCSC barred him from provincial capital markets for life.

Sharp, his associates, and affiliated offshore entities took down 70% of the financing, with Fortuna’s network subscribing to another ~19% of the placement. The Sharp-connected investors were a group of documented fraudsters: Paul Sexton of the ‘Veldhuis Control Group’ – who received the largest individual monetary order among five BC residents in a $168.9 million aggregate penalty – as well as Ardent Strategies Corp., whose accounts the SEC froze across seven entities. Six offshore entities sharing addresses located in a documented node in Sharp’s platform subscribed.

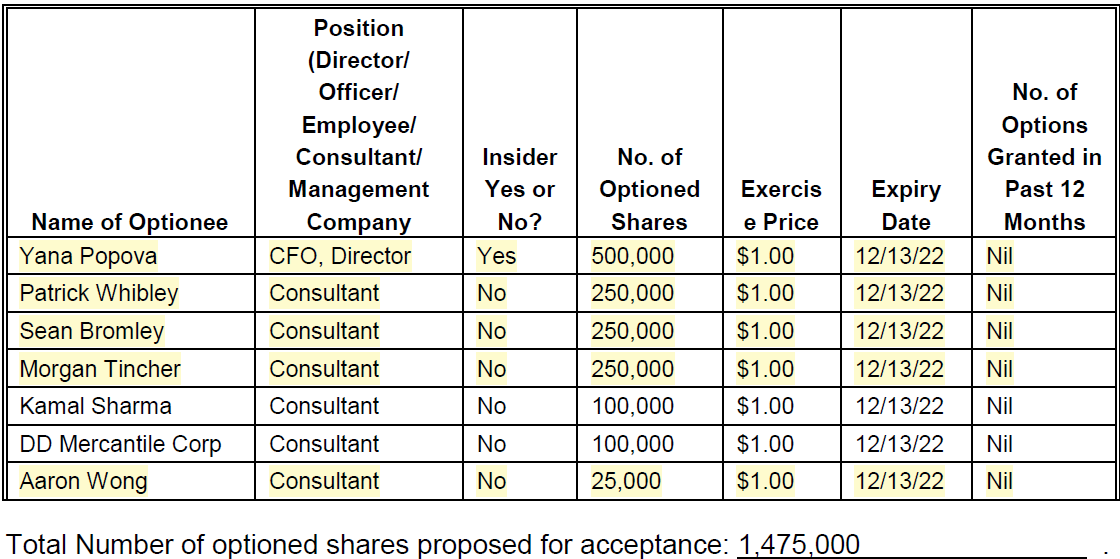

With cheap equity secured, Fortuna began to tighten its grip on Atlas’ operations. In November 2017, Atlas appointed Yana Popova, a key member of the Fortuna nexus, as CFO/Director. A month later, Fortuna’s Sean Bromley, then 27 years old, was appointed to the board. Invictus IR, run by Fortuna affiliate, Walter Spagnuolo, was granted 300K options to provide Investor Relations services.

On the day of Bromley’s appointment, Atlas granted ~1.5 million options, with ~1.3 million going to Fortuna’s network, including Bromley, Popova, Patrick Whibley, Morgan Tincher, and Aaron Wong. A 2018 archive of Fortuna’s website shows these individuals as part of its “team”. Tincher, the only member of the network not listed, is a repeat consultant across Fortuna promotes.

Atlas then began its push for attention from retail investors. In late 2017, the company announced the acquisition of a 6,600 sq ft data center in Washington State, touting cheap local electricity and plans for a 5.0MW crypto mining operation. Over the following eight months, investors received a steady drip of updates — refurbishment underway, renovations complete, power energization pending — with full operations perpetually just around the corner.

With catalysts on the horizon, Atlas spent heavily on stock promotion. For the year ending May 2018, it spent ~$917K on promotion “to inform the industry and current and potential shareholders of its entry into the cryptocurrency industry”. Between May and November 2018, Atlas dished out almost $1.2 million for promotion.

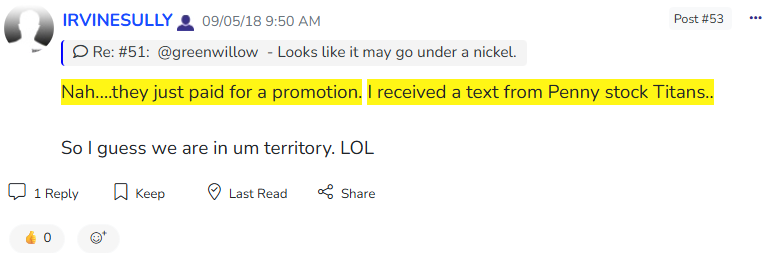

As a result, Atlas’ stock surged and the OTC exchange requested they comment on the price action. Atlas disclosed a PR from Monster Media may have driven the rise, revealing it had paid for stock promotion from a lost list of consultants in the prior twelve months: Marco Messina, Monster Media, Invictus IR, Full Service Media, Resultz Media, Khaos Media, and Bull Markets Gmbh. Companies that engage Marco Messina frequently have had to respond to OTC requests for commentary on their stock promotion campaigns [see examples, 1,2,3]. An investorshub.advn user also flagged paid promotion from Atlas, mentioning a text they received from “Penny Stock Titans”.

Almost a month after paid promotion sent its stock soaring, the hype around Atlas reversed. It did what any reputable bitcoin miner seems to do and left the business entirely, citing “uncertainty of the bitcoin mining market and “efforts to increase shareholder value.”

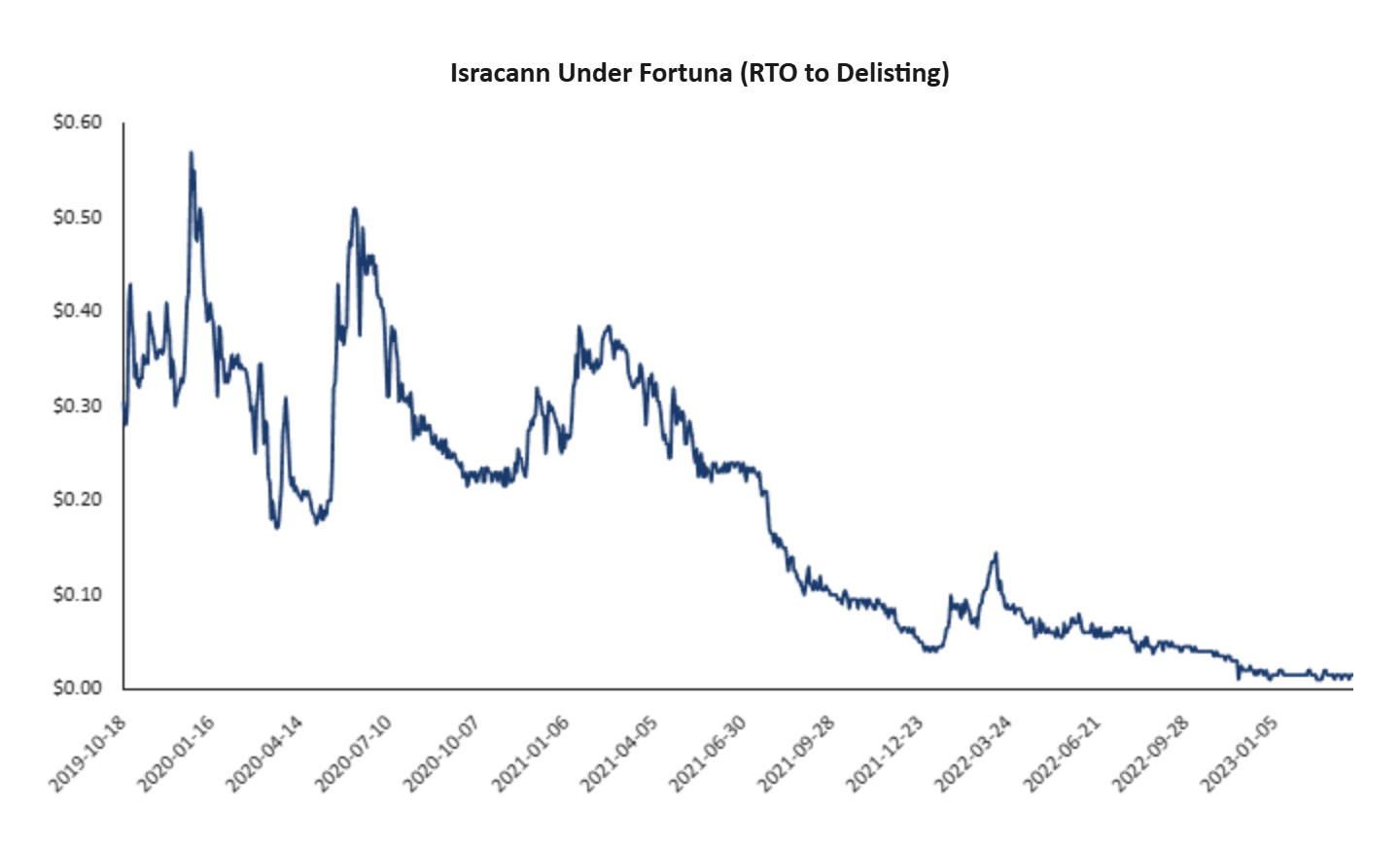

Case Study 2B – Isracann: Puff Puff Promote

Having torched Atlas’s credibility on crypto, Fortuna pivoted to cannabis – a sector attracting billions in capital on the back of legislative tailwinds. It orchestrated a reverse merger between Atlas and Isracann Biosciences (CSE: IPOT) (“Isracann”), a company purportedly seeking to farm cannabis in Israel at an industrial scale.

Isracann was incorporated in Canada just months before it signed a binding letter of intent with Atlas in October 2018. It had no operating history, and the Israeli farming entity it was built around wasn’t even incorporated until months after the deal was announced. This was, in substance, a merger of two shells. Fortuna was handed 2.3 million shares for brokering the deal

With the reverse merger pending close, in February 2019 Isracann quietly issued 42 million shares at $0.01 to undisclosed investors. Eight months later the deal closed and those shares were exchanged for Atlas stock at a deemed value of $0.50, implying a company with no operating assets or history was suddenly valued at $23 million. In just months, the undisclosed investors had netted a 38x paper gain. They also received 28 million free warrants at a ~$0.05 strike price as part of the merger. We have seen this structure – cheap shares issued to undisclosed insiders ahead of a liquidity event (RTO or IPO) – repeatedly across Fortuna companies.

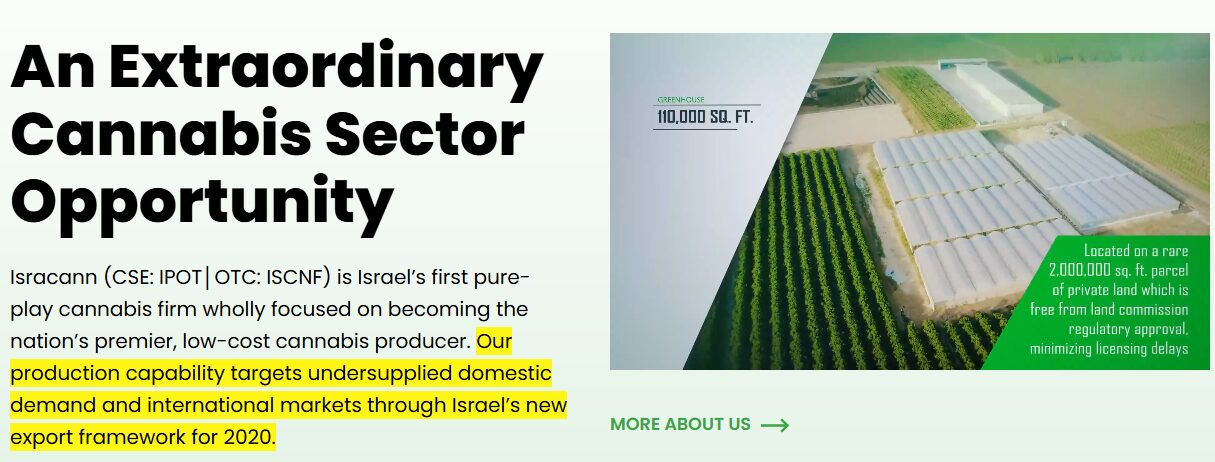

Isracann branded itself as Israel’s “first pure-play cannabis firm”. It announced plans to build four greenhouses, totaling 230K sqft and ~23,000 kg of dry flowers. The Company sought to begin construction of its first two facilities in Q4 2019, with cultivation and harvest in 2020.

Despite the capital required to break ground, Isracann’s priority was its stock price. The day before the company had even resumed trading on the CSE (post-Atlas merger), it agreed to pay ~$840K for services from a laundry list of promoters: BlackX GmBH, CFN Media and Equity Guru, Mountain Capital, Dig Media, Business Television (BTV), Invictus and Stonebridge Partners. This was just the start of an all-out blitz to pump the stock.

In October 2019, Isracann signed a ~$800K agreement with CDMG, Inc. an advertising agency specializing in direct mail and digital marketing. In January 2020, it paid them another $824K and engaged Promethean Marketing for $200k. Promethean was run by William “Bill” Kaitz, who was named in the SEC complaint against the Sharp Group that alleged he went beyond simply promotion and served as a specialist in exit liquidity, touting stocks that insiders simultaneously planned to sell, while concealing their involvement. The SEC ordered him to pay $1.3 million in civil penalties.

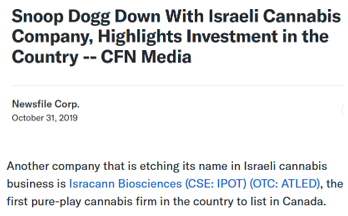

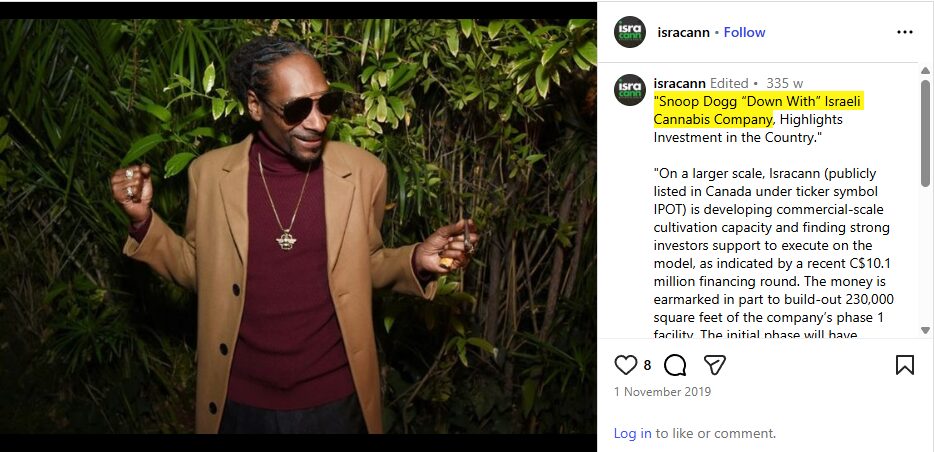

The promo was frequently misleading. A common tactic: take tangential news, lead with it, and weave Isracann’s name in deceptively. In October 2019, Snoop Dogg invested in Seedo, an Israeli cannabis company with no affiliation to Isracann. Isracann’s consultants nonetheless ran headlines designed to make investors believe Snoop had backed Isracann. The company itself amplified the confusion on its Instagram page.

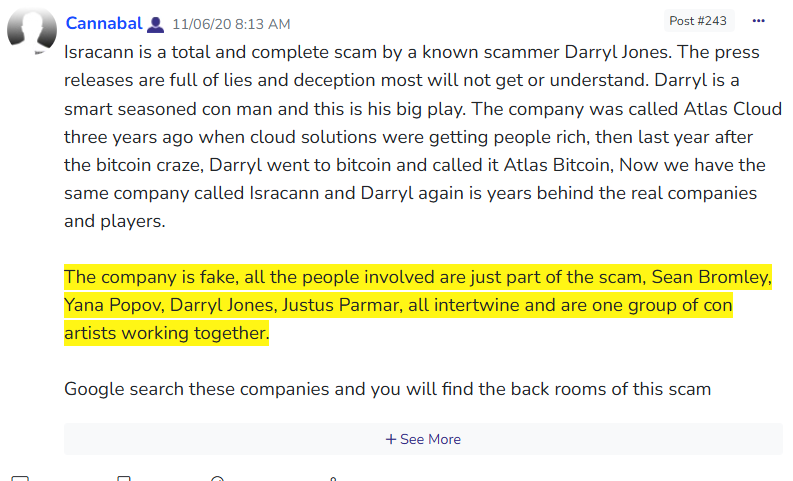

None of it translated into operations. In April 2020, Isracann disclosed it had yet to break ground on any facilities, despite having guided for cultivation to begin that quarter. By May 2020, its only operational milestone was a $2.7 million acquisition of 50% of Cannation, an Israeli company owning two farms. Retail investors were growing vocal. Online posts described the company as “fake” and called the Fortuna network “one group of con artists working together.”

The promised Nir Yisrael greenhouses were never built. In October 2021, the company placed the project on hold. After failing to generate any revenue, it pivoted yet again, acquiring Praesidio Health, a Canadian natural health products (NHP) company but that never went anywhere either. A Management Cease Trade Order (MCTO) was imposed by the BCSC in February 2023 for Isracann’s failure to timely file its financials after having previously received another MCTO. It was never cured and Isracann was ultimately delisted from the CSE. Shareholders got left holding the bag.

Throughout the promote, the Fortuna network collected equity. Yana Popova and Sean Bromley served as executives and directors for the duration. Matt Chatterton was appointed COO in June 2020 and later became Chief Science Officer at Praesidio.

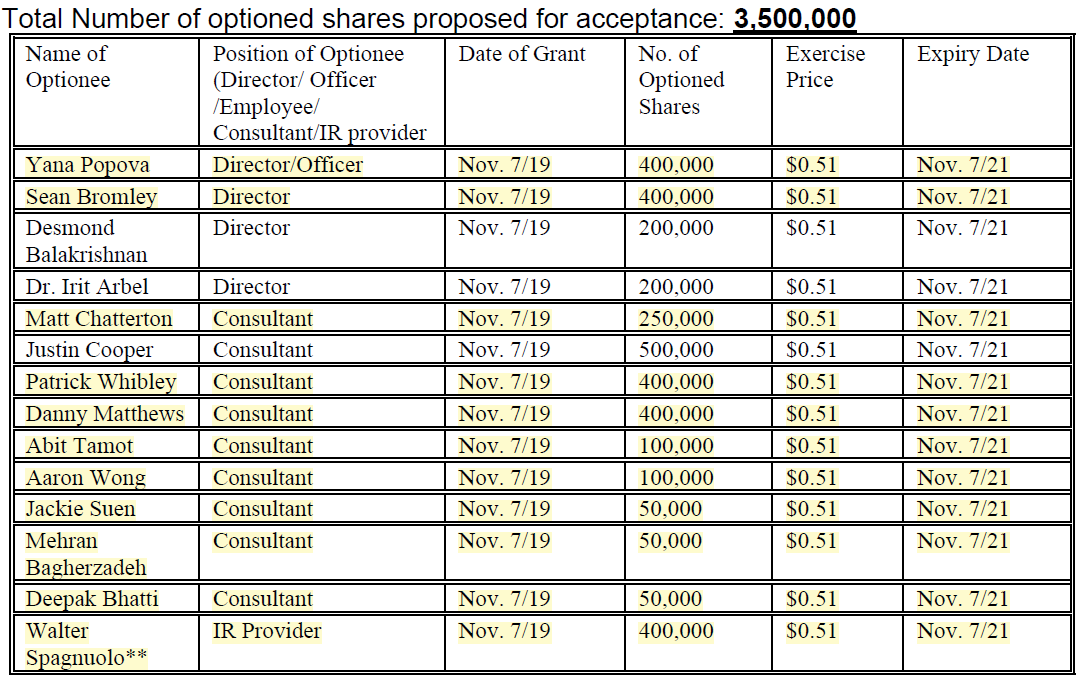

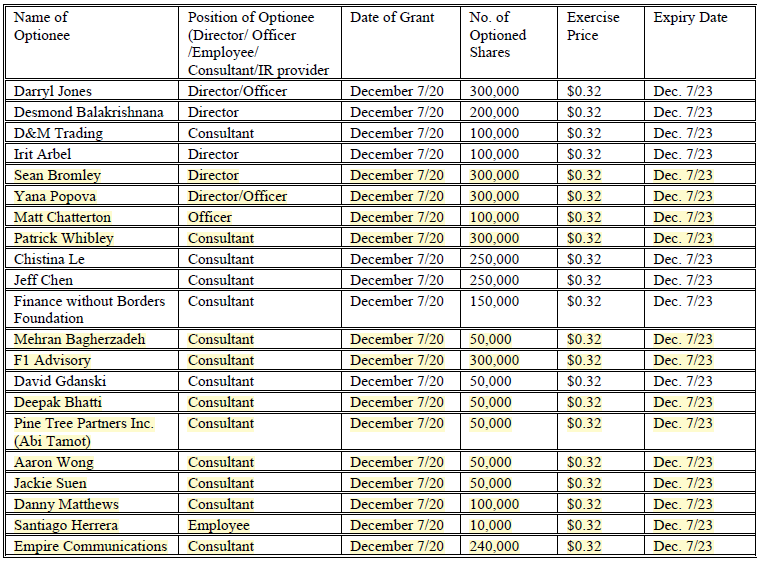

The network was paid regardless of how the business performed. Just one month after the Atlas merger closed, Isracann issued 3.5 million options at a $0.51 strike to Bromley, Popova, and affiliates — including active Fortuna employees and IR consultants Mehran Bagherzadeh and Walter Spagnuolo. A further ~3.3 million options were issued to the network in December 2020, including 300K directly to Fortuna (F1 Advisory).

Case Study #3 – Pacific Rim Cobalt: Cobalt Mania and Paid Promo from a Goldman Sachs Lookalike Couldn’t Prevent 99% Decline

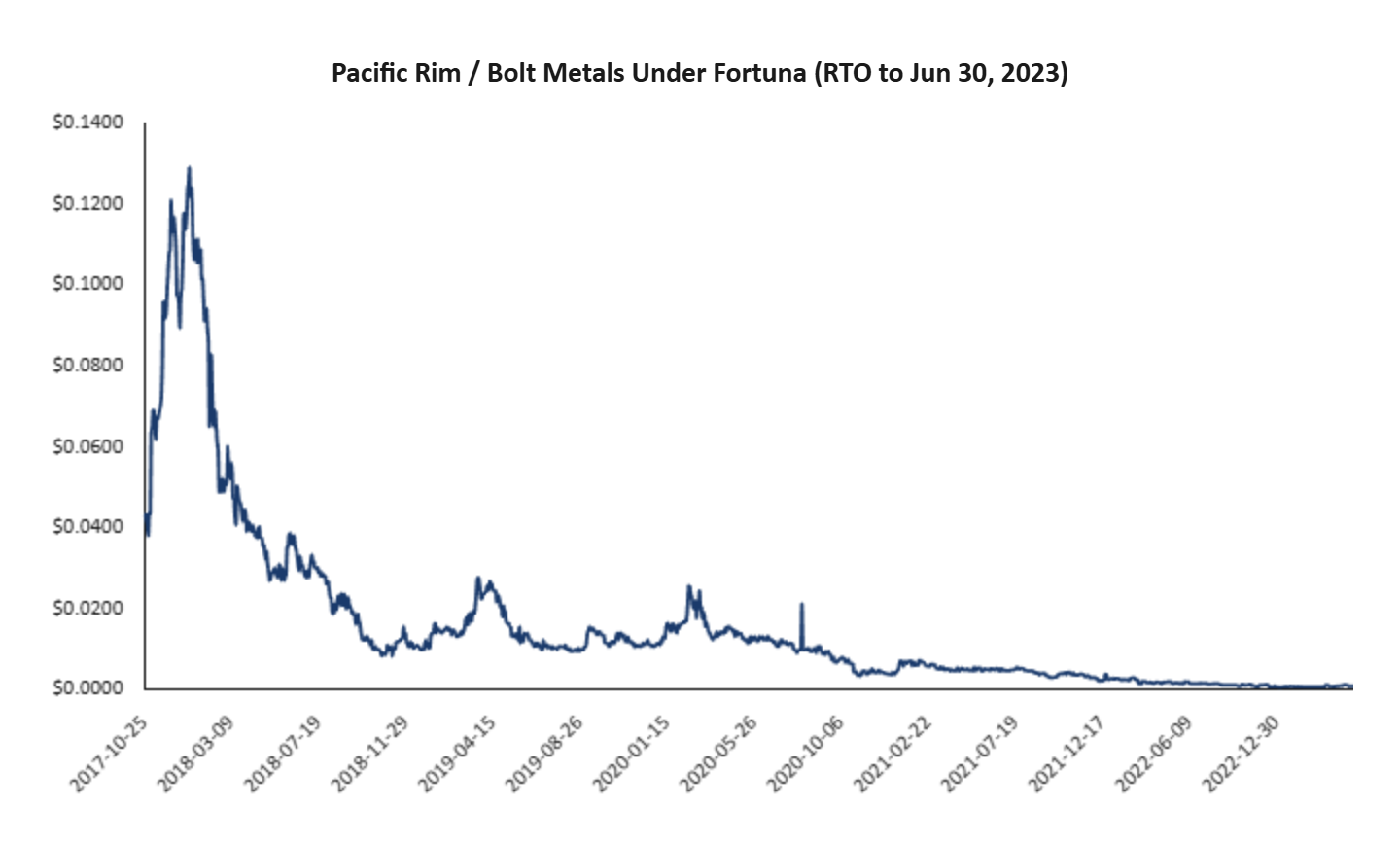

Pacific Rim Cobalt Corp. (CSE: BOLT) (“Pacific Rim”; later “Bolt Metals”) was an aspiring Indonesian cobalt explorer which came public through a Fortuna-led reverse merger with dormant shell, Rhys Resources. It debuted just as cobalt prices tripled on EV battery demand projections, making junior cobalt plays among the hottest names on Canadian exchanges.

A November 2017 press release credited “Fortuna Investment Corp. and Delano Capital Corp.” as the firms that had “structured the Company’s initial capital raise.” Delano Capital Corp. is led by Julian Bharti, son of serial Canadian stock promoter, Stan Bharti (“Stan”). He was a Managing Director at his father’s merchant bank, Forbes and Manhattan. Stan was sued in Ontario for his stock promotion schemes and has a history of bringing stocks that collapse to the public markets. Stan ran a fund called Routemaster which also owned shares of Pacific Rim.

The Fortuna roster was fully assembled. Bromley was installed as director, handling IR through his Parmar Group email. Patrick Whibley was a consultant. The appointed CEO, Ranjeet Sundher, was a repeat Fortuna name, who would later resurface as CEO of Tactical Resources (TSXV: RARE).

The story centered around Pacific Rim’s TNM Cobalt Project which the company touted as uniquely positioned in a region with the largest source of cobalt outside Africa and strategic location next to China, the world’s largest cobalt buyer. Located in Papua Province, Indonesia, the asset was 5,000 hectares where historical operators had drilled 856 holes in the 1970s and 1980s.

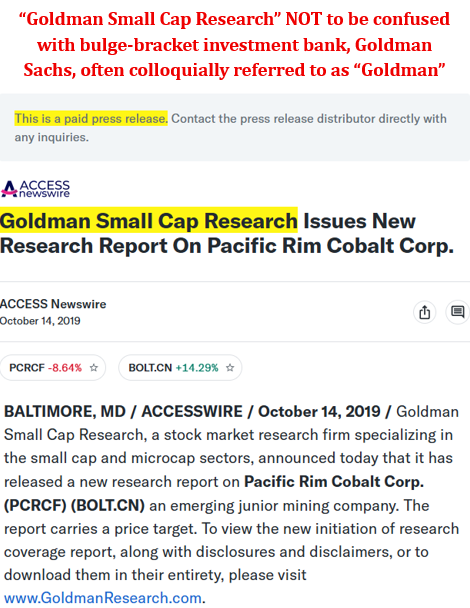

In April 2018, Pacific Rim mobilized two drill rigs and CEO Sundher promised a maiden resource estimate “in the near future”. As investors waited, Pacific Rim pressed heavily on stock promotion, sponsoring articles from outlets like FinancialBuzz.com and Microsmallcap.com on “cobalt’s scarcity” and how rising cobalt prices “might just be getting started.” Similar to the Snoop Dogg promotion at Isracann, these articles would often cite other companies to confer credibility, or reference outlets such as “Goldman Small Cap Research” (see Goldman Small Cap Research Issues New Research Report on Pacific Rim Cobalt Corp.) which was, in fact, totally unaffiliated with the investment bank, Goldman Sachs, despite the intended connotation.

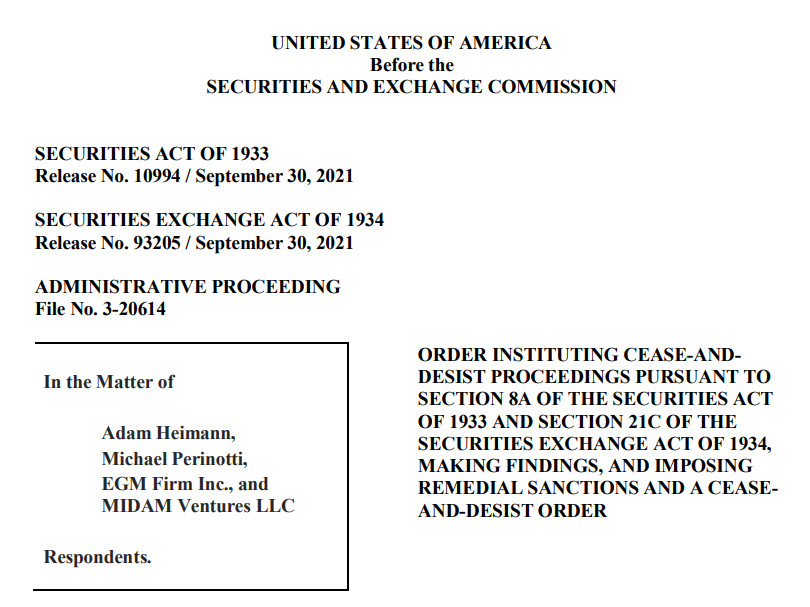

The company also hired Midam Ventures and Fortuna affiliate Aaron Wong as part of a “shareholder communication initiative.” In 2021, the SEC issued Midam a Cease-and-Desist Order for misconduct across ten microcap promotional campaigns between 2015 and 2018, alleging its principals engaged in manipulative trading and failed to disclose promoter compensation accurately. Midam was also engaged at Reliq Health Technologies (TSXV: RHT) – the company ushered public by Parmar and Shane Parhar, detailed earlier in this report.

As the hype cycle went on, Pacific Rim struggled to keep its books in order. In May 2019, a Management Cease Trade Order was imposed for failure to file annual financials. Ultimately, no NI 43-101 compliant resource was ever produced. The promised maiden resource never materialized despite two drill programs and years of press releases about transformative potential.

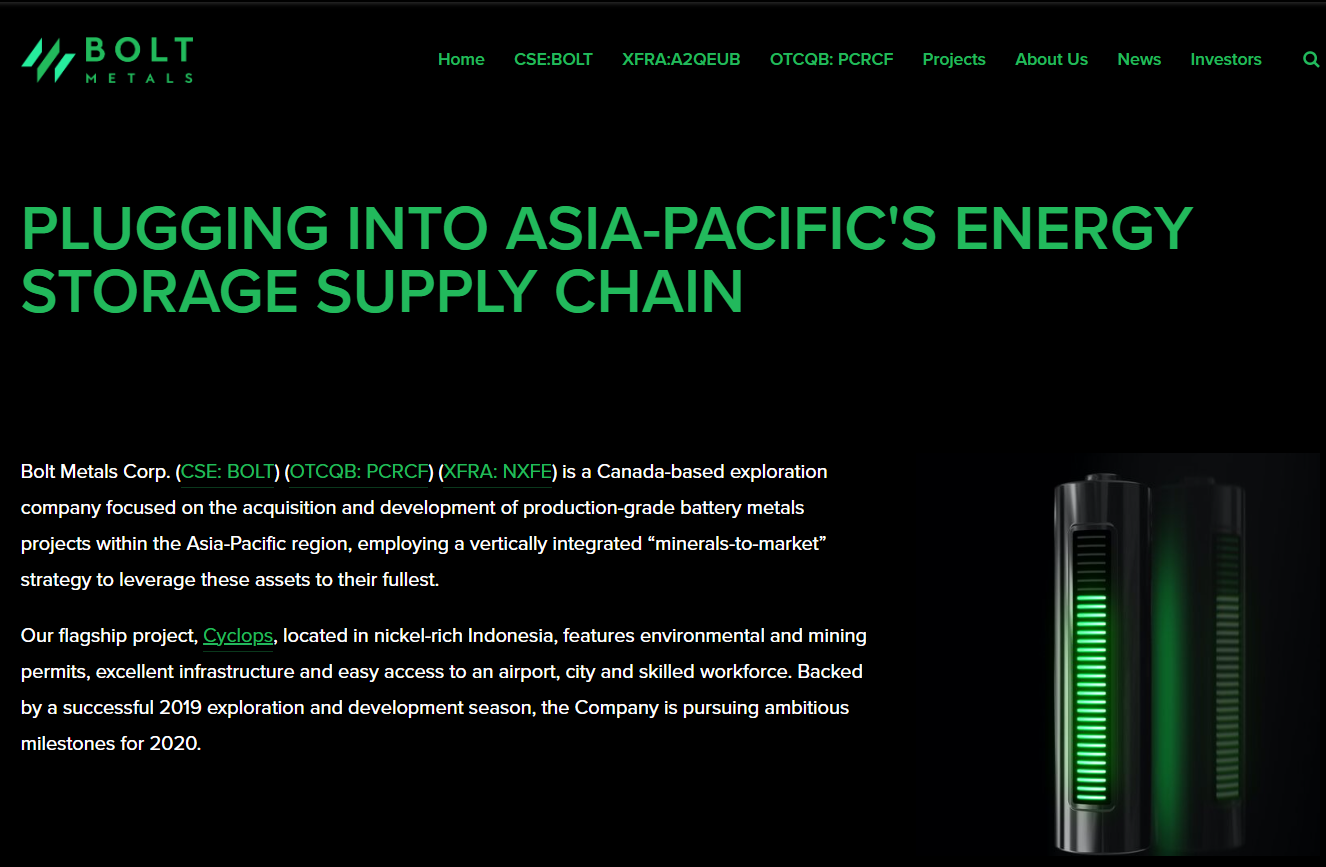

When cobalt prices crashed and the theme fell out of fashion, Pacific Rim did what Fortuna companies do: it rebranded. It dropped “cobalt” from its identity, renamed itself Bolt Metals, and pivoted to Indonesia’s nickel reserves and EV supply chain ambitions. Same story. New ticker.

The pivot changed nothing. In February 2022, the Indonesian government revoked Bolt Metals’ mining permit as part of a mass cancellation. The company’s sole asset was gone. Bromley remained listed as director and investor contact for seven years, overseeing a 99% decline.

Starfighters Space: “Next Frontier”, Same Old Story

Taking the Crew to Space

To his credit, Parmar has a genuine talent for spotting emerging themes, getting in early, and structuring stories he can profit from when retail liquidity arrives. He was in crypto before the boom, cannabis ahead of the legalization wave, cobalt as the EV frenzy was building. But as these case studies have shown, by the time the company is public the easy money has usually already been made. It turns out that there was never much of a business to begin with. Parmar and Fortuna move on to the next.

Fortuna identified space as “the next emerging industry to target” as early as February 2022, months before it was formally engaged by FJET. When Parmar publicly announced his US expansion in February 2023, he confirmed FJET as Fortuna’s first space investment, stating that “the space industry really is the next frontier.”

Fortuna appears to have been introduced to FJET by an old friend. Crystal Carson, a self-proclaimed “trailblazer, connector, and entrepreneur”, describes the deal as her first “origination.” In 2024, she was taken on a private jet with the Fortuna team to the Space Symposium. She recapped the event again describing it as the “first deal [she] originated”.

The connection to Carson traces back to Vancouver years ago. She reported at Mackie events for FinancialBuzz.com, an outlet that promoted several Fortuna companies, and was an advisor to Promino Nutritional Sciences (CSE: MUSL), a Fortuna penny stock where affiliates including Sean Bromley were also involved.

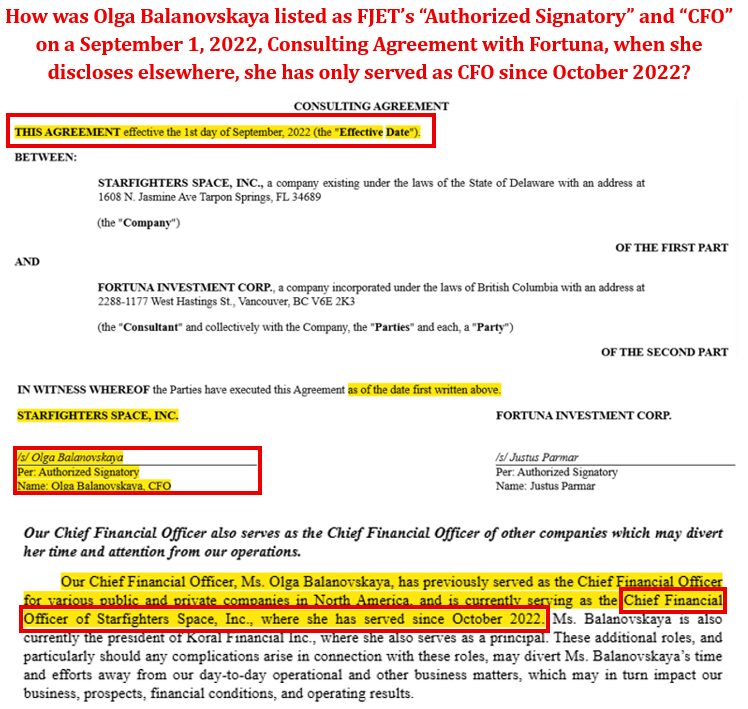

Fortuna was formally engaged as a consultant by FJET in September 2022. The consulting agreement was signed on FJET’s behalf by Olga Balanovskaya — herself a Fortuna affiliate — a full month before filings indicate she formally joined FJET as CFO. How she was authorized to bind a company she had not yet joined is unexplained.

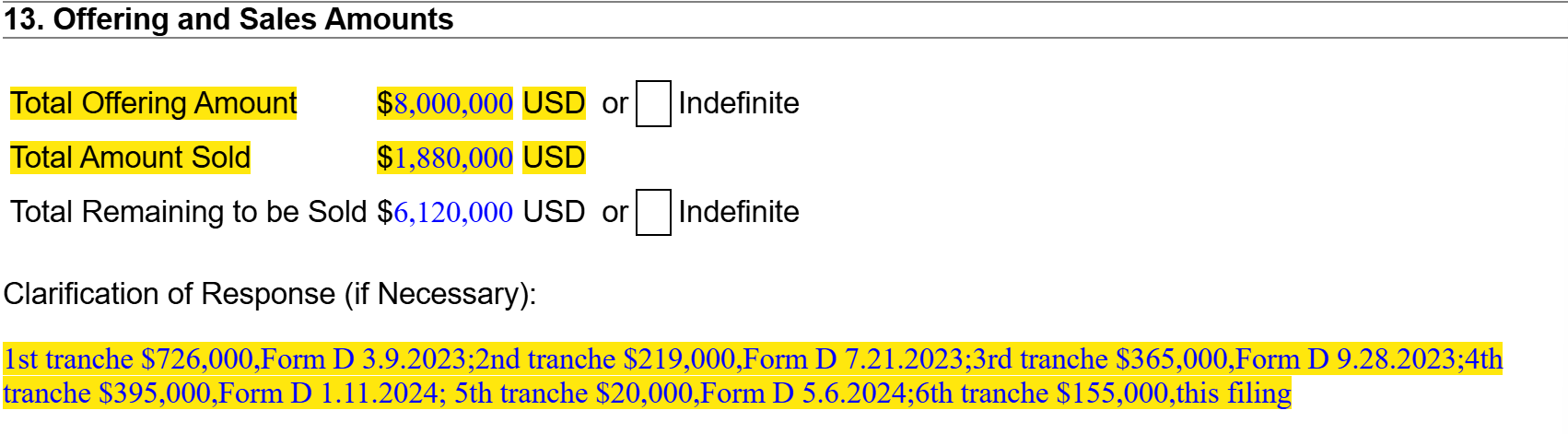

Unlike its previous promotes, Fortuna did not take FJET public via a reverse merger. Listed as a “Promoter” on FJET’s Form D filings from late 2022 through late 2024, Fortuna attempted to raise $8 million from accredited investors through private placements. Parmar has touted that Fortuna “did extremely well in the battery technology space”. That proven track record would presumably enable the firm to raise a mere $8 million over two years, especially in the space sector which drew roughly $7 billion in capital in 2023 alone. However, Fortuna raised just $1.9 million across several tranches: a 76% shortfall.

Facing that wall, they pivoted to a Reg-A offering with EquiFund in January 2024, requiring a minimum investment of just $718. Fortuna couldn’t raise $8 million from sophisticated investors went so it went to the public at less than $1,000 a ticket with its “unique pre-IPO investment opportunity.”

As we saw in the Isracann case study, Fortuna companies frequently issue cheap equity ahead of an liquidation event. FJET is no exception. While retail investors are piling into the space “story” today, Fortuna’s economics appear to have been locked in long before the IPO. Fortuna received retainer-based payments from the company, but the promote seems to have been structured around 18.15 million warrants which were acquired for $0.01 per warrant in September 2022 and Sep 2023. The warrants had a $0.33 strike price, ~90% below the IPO price of $3.59. While the investors information is redacted, the top 3 holders took almost ~11.8M warrants with the largest holder taking ~5.8M warrants.

Upon engagement, Fortuna began drawing from its roster. Aerospace has huge barriers to entry, but – as with e-mobility, crypto, cannabis, cobalt before it – Fortuna chose a team with no meaningful experience in the industry. The recent resignation of Rick Svetkoff — FJET’s founder, the one person at the company with decades of F-104 experience — makes the void that much more problematic.

At the board level, Fortuna installed its go-to-guy, Sean Bromley, who remains a director today. Austin Thornberry – who has cycled through CFO roles at Three Sixty Solar (delisted), UniDoc Health (collapsed), and The Vurger Co. (insolvent) – was appointed too, before quietly resigning from his post just before the IPO. Frostee Rucker, a retired NFL defensive end, who serves as VP of Sports & Entertainment at Fortuna stepped down from the board at the same time. Rucker’s role is to facilitate “introductions to his extensive network of professionals, athletes, and celebrities.”

Following Svetkoff’s resignation, the board appointed Tim Franta as CEO. Franta holds a BA in English Literature from Flagler College. In a profile published by his alma mater, he said: “The biggest thing I learned at Flagler was how to tell a story.” Before Starfighters, Franta was Deputy Director of Energy Florida, a nonprofit, and an award-winning film producer whose credits include an Emmy-nominated documentary about a Star Trek actress. He has no engineering degree, zero propulsion experience, and lacks an aerospace background of any kind.

FJET’s CFO, David Whitney, was appointed January 2024 — and operates out of Vancouver, far from FJET’s Florida and Texas operations. Prior roles include CFO of a fintech rental payments startup, a property management software company, and BRON Studios, a Canadian film studio that went bankrupt. His biography omits that he was also CFO of Abattis Bioceuticals from February to May 2018, directly replacing Anthony Jackson — one of the primary architects of the Bridgemark Group stock manipulation ring. Like Franta, Whitney has no aerospace experience whatsoever. Within weeks of the December 2025 IPO, Whitney sold 37,500 shares at $9.97 per share for $373,875.

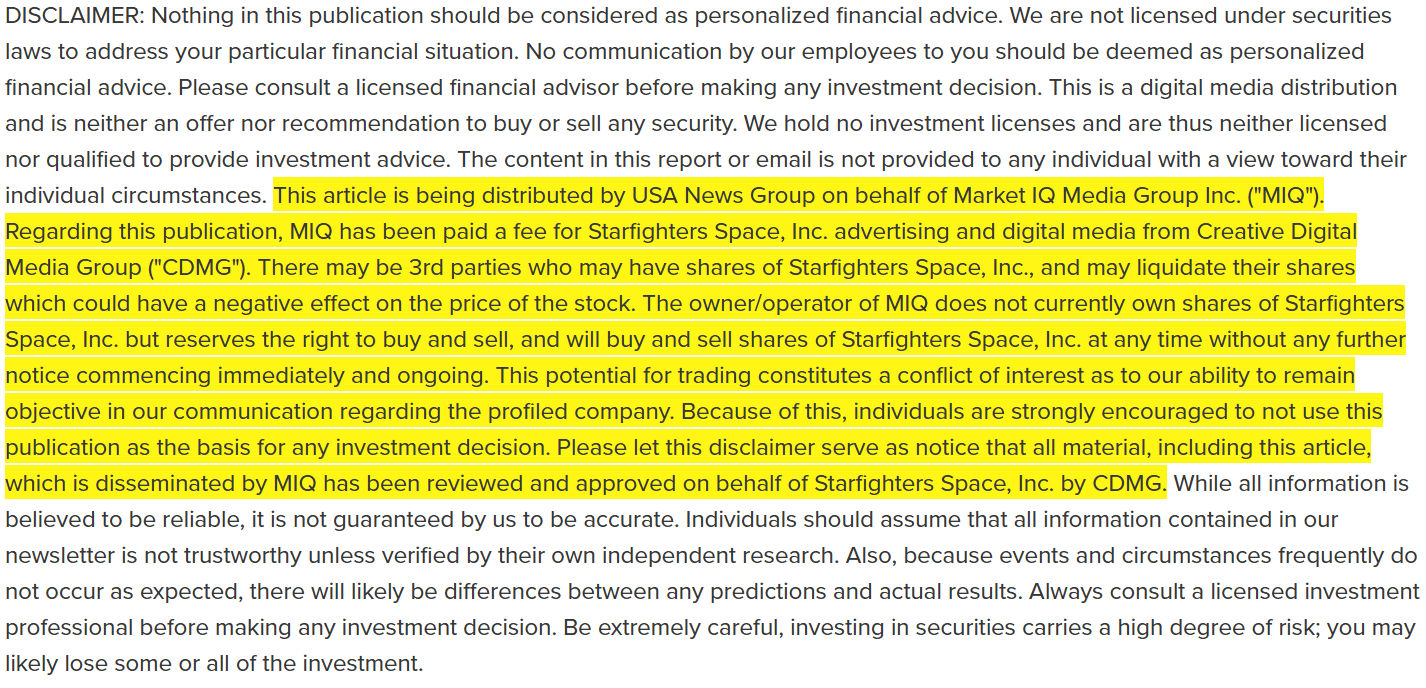

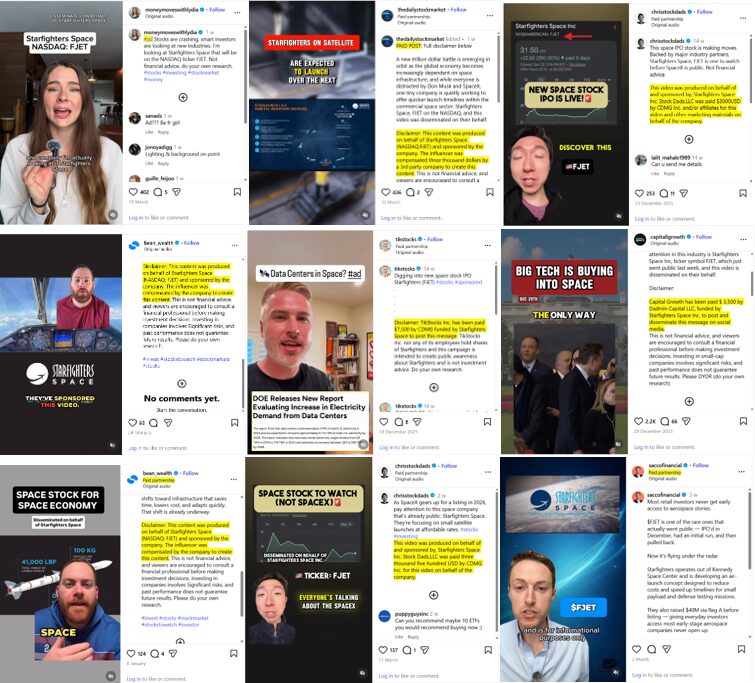

FJET’s Stock Promotion Network Includes a Firm Whose Principal Has Been Described as Having “A History of Promoting Scams Targeting Seniors”

In the lead-up to the IPO, Fortuna introduced retail financial media outlets like WOLF Financial to FJET, sponsoring events at Nobu and field trips to the Kennedy Space Center.

Since coming public, FJET continued to pay for relentless stock promotion which closely mirrors the deceptive style prevalent in its past companies. These fluff pieces insert FJET in commentary on defense spending and space exploration alongside SpaceX and Northrop Grumman, while tagging other high-flying stocks like Archer Aviation (NYSE: ACHR), Intuitive Machines (NASDAQ: LUNR), and AST SpaceMobile (NASDAQ: ASTS) to capture retail investor attention.

In 2023, FJET signed a consulting agreement with Caleb Huey of Creative Digital Media Group (CDMG). As compensation, Huey received 2.75 million warrants with a $0.33 strike price, along with $150k in cash. CDMG has funded social media promotions and distributed paid articles [examples 1,2,3,4] via USANewsGroup.com on behalf of Market IQ Media Group (“MIQ”), another BC-based promotion firm which other Fortuna companies have used and whose principal has invested alongside the firm.

Caleb Huey’s father, Craig Huey, is listed as CDMG’s founder and CEO and is described as having a “history of promoting scams and deceptive schemes, including fraudulent investment and nutrition products targeting seniors.” An exposé on his past provides insight, including his promotion of 47x return potential on a gold miner that was labeled a “pump-and-dump scam” before its stock collapsed. CDMG is engaged at other Fortuna companies, including Tactical Resources Corp. (TSXV: RARE) and Eagle Nuclear Energy Corp. (Nasdaq: NUCL).

FJET has also paid for stock promotion from Dadmin Capital, LLC., an entity run by Austin Wynn. Damin Capital has marketed the collapsed stocks of a long list of clients, including LiveOne (Nasdaq: LVO), Splash Beverage Group (NYSE American: SBEV), and KULR Technology Group (NYSE American: KULR).

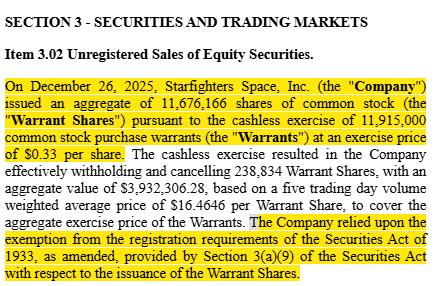

On December 26, 2025 – just four full trading days after IPO – FJET announced 11.9 million of the warrants were converted via cashless exercise, resulting in the issuance of 11.7 million shares. The holders used a cashless exercise feature to exempt them from having to register the warrants for resale. A Form 4 filed by Sean Bromley at the same time confirms the warrants were likely held within the Fortuna network. Based on the 5-day VWAP of $16.46 per share at the time of exercise, the deal represented ~$192 million in share value extracted.

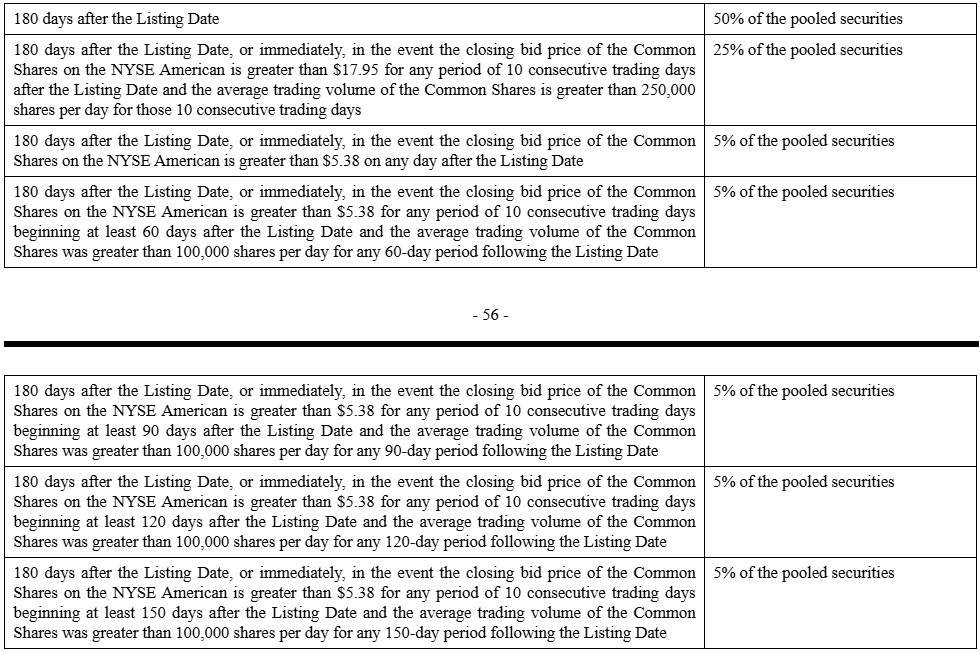

A further 6.6 million warrants remain unexercised. The 18.5 million warrants and another 3.8 million in shares issued to debenture holders are subject to are subject to a lock-up agreement with price and volume-based triggers. Based on these conditions, we estimate 15% of the securities (3.3 million) have been unlocked. If current price and volume conditions continue to be met, another approximately 1.1 million shares unlock on April 16, followed by a similar tranche on May 16. The largest release, approximately 16.8 million shares, unlocks on June 15, 2026, when the 180-day hard lock expires.

A Rocket Launch Developer with $0 Spent on R&D For 3 Years; Currently Spending 3x More on Consulting Fees Plus Travel & Entertainment Expenses

Comparing FJET’s rampant paid promo to its other operating expenses reveals it has prioritized marketing its stock over developing rockets. Contract labor and fuel costs – the closest proxy for actual flight activity – have stayed flat at $400–500K since 2022. Meanwhile, the Company reported $0 (nil) in R&D expense from 2022 to 2024. Three consecutive fiscal years of zero R&D while claiming to develop an orbital launch rocket with GE Aerospace. The first R&D spending of $636K appeared only in the first nine months of 2025, coinciding with the IPO process. Over the same period, consulting fees totaled $2.06 million and travel and entertainment added $1.14 million.

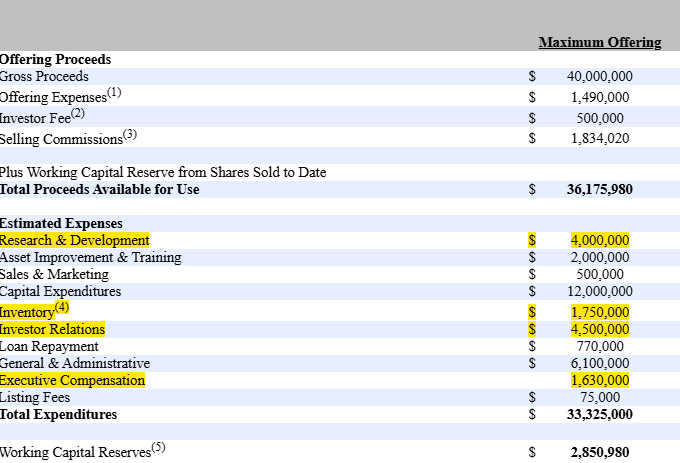

Documents from FJET’s IPO shows that it planned to spend more on investor relations than it would on R&D in a maximum offering scenario. In a scenario where FJET did not raise its maximum offering, inventory – defined as “primarily StarLaunch I rockets and related equipment” – received an allocation of just $500K of the total proceeds.

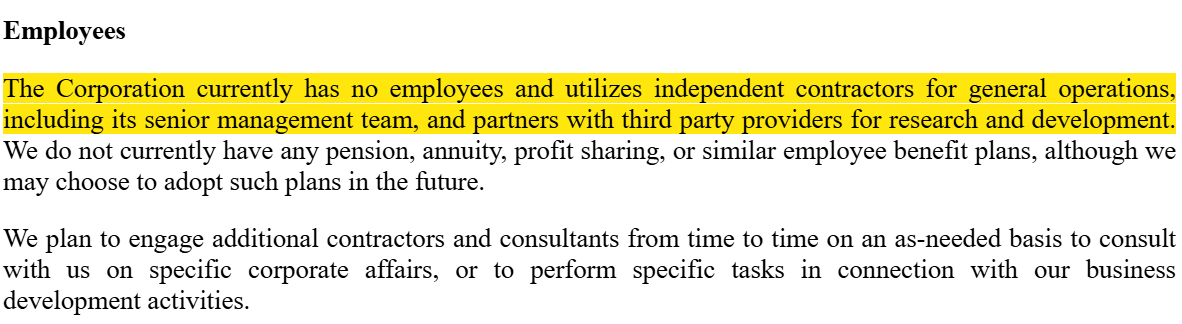

The expenses check out with the rest of FJET’s business. Its offering circular discloses that it has zero employees. All personnel are independent contractors. The VP of Operations works 20 hours a week while simultaneously flying commercial routes as a Southwest Airlines captain. Beyond the executive team, just one aircraft technician and a recently graduated Director of Marketing work with FJET. There are no open job postings.

Taken together, the structure at FJET is highly reminiscent of Loop Atlas, Pacific Rim, Isracann, and countless other names in Fortuna’s wake. A retail-friendly theme. A recycled network. Cheap equity secured long before the public arrived. Paid promotion to keep the story alive. And a company that shows scant signs of existing. Part 2 examines what Starfighters is actually selling and whether any of it holds up.

Part 2: Starfighters Has No Rocket, No Engineers, and No Path to Launch

Mach 2 Dreams: What Starfighters Tells Investors

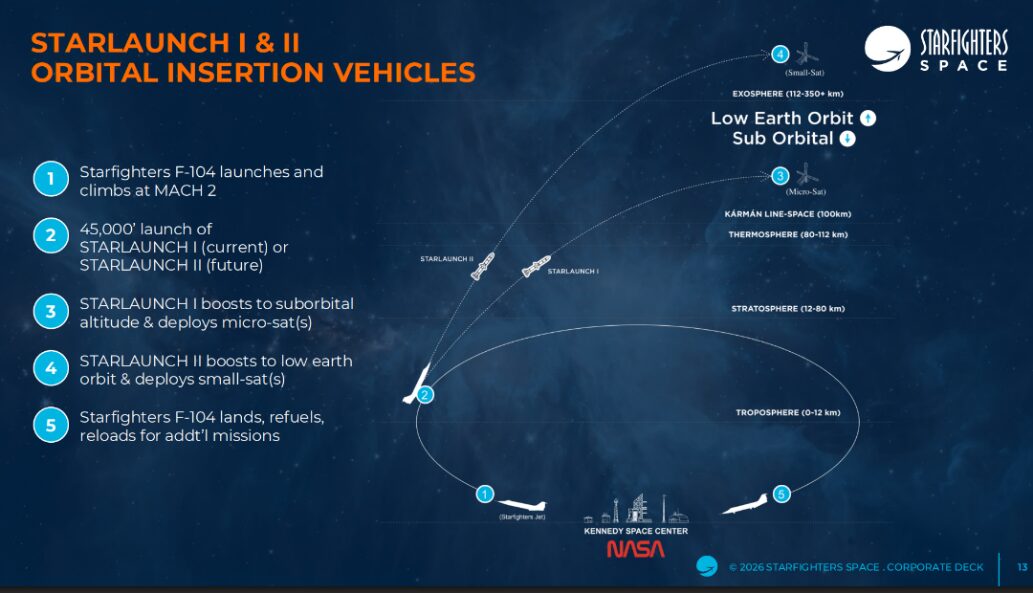

Setting Fortuna’s playbook aside, the FJET story is about using seven F-104 fighter jets to carry and air-launch rockets from high altitudes at supersonic speed, eliminating the need launch pads, derricks or cranes. The Company claims to have two proprietary air-launch rockets in development: Starlaunch I and Starlaunch 2.

The concept is simple: an F-104 climbs to Mach 2 at 45,000 feet, releases a rocket from its wing, and returns to base while the rocket carries the payload to orbit. FJET says this has three advantages over ground launch: lower cost, scheduling flexibility, and global reach.

While air launch may theoretically have the advantages FJET promotes, the Company’s claims about its own carrier aircraft and rocket platform are all either highly misrepresented or completely made up.

FJET’s program materials describe the F-104 as a “proven first-stage launch vehicle with thousands of missions over 60 years.” This is false. NASA operated eleven F-104s over 38 years, used predominantly for experimental flight testing and never as an orbital launch vehicle. The only documented instance of an F-104 launching a rocket was NASA’s ALSOR (Air Launched Sounding Rocket) program from 1959 to 1962. Five rockets were launched before the program eventually concluded that the F-104 was “temperamental”. It was abandoned after being destroyed in a crash in December 1962.

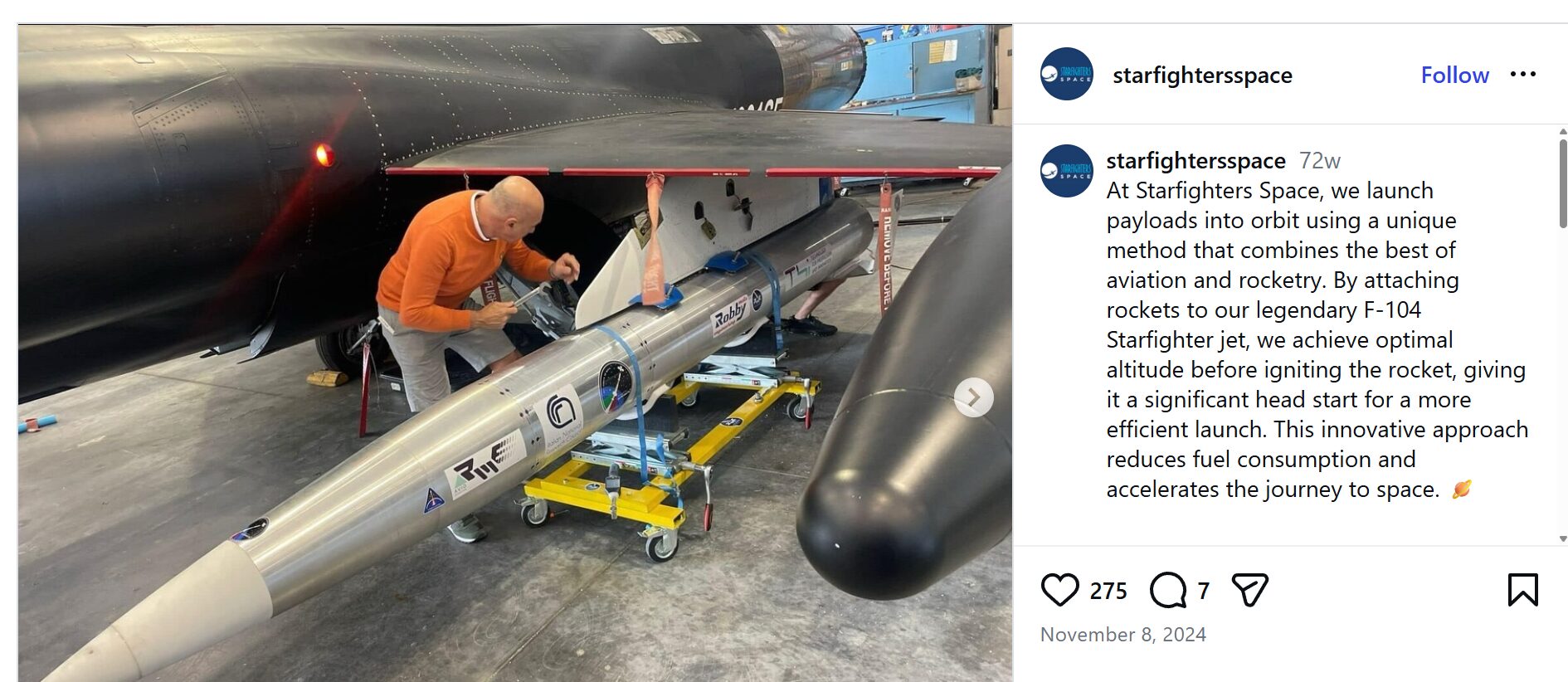

Since Fortuna was engaged at FJET, the Company has relied upon two marketing slides as renderings for its StarLaunch I and StarLaunch II rockets. Both renderings are modified stock artwork. The StarLaunch I image is concept art of the AIM-120 AMRAAM by an artist named Edgar B. FJET left the original serial number on the missile body and tacked on an American flag. The StarLaunch II image is a 3D render of a “long range missile starting engine” by Alexandar Yartsev, available to be purchased for $2.90 at Shutterstock. Claiming to build “the most efficient and cost-effective small payload rocket in the world”, FJET has not even produced its own rendering…

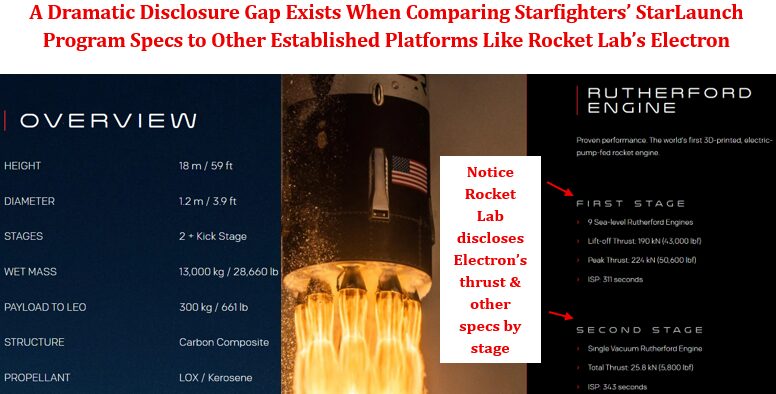

FJET also never discloses industry standard technical specifications, including propellant type, specific impulse, total rocket mass at ignition, per-stage thrust, number of stages, and more. These are not some obscure engineering details, but rather the key determinants of a rocket’s performance. For perspective, Rocket Lab publicly discloses all of these metrics and more.

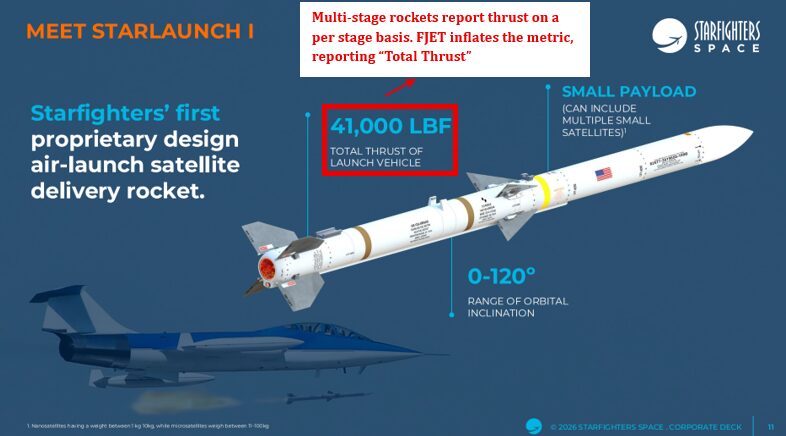

The specs FJET does provide are reported in a non-standard way that makes no sense. Its February 2026 corporate presentation reports “total thrust” as opposed to thrust per-stage. It sets StarLaunch at 41,000 lbf of “total thrust” and Starlaunch II at 111,000 lbf.

Reporting “total thrust” is misleading because rocket stages fire sequentially, not simultaneously. No multi-stage rocket produces its total cumulative thrust at any single point in flight. While three stages of 20,000, 15,000, and 6,000 lbf sequentially may equate to a cumulative thrust of 41,000 lbf, the maximum thrust produced across those stages is 20,000 lbf. Stage 1 thrust is cited most frequently as it determines whether a rocket will actually fly.

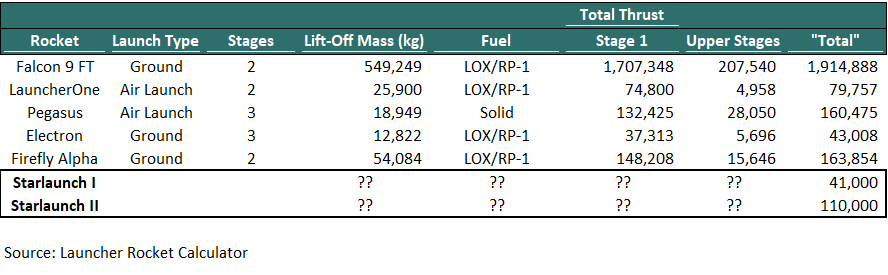

FJET reporting 41,000 lbf does not pass the sniff test. If we apply FJET’s “total thrust” methodology to Rocket Lab’s Electron it would have 43,008 lbf of total thrust, nearly identical to StarLaunch I. It makes no sense for these two programs to have comparable thrust as the Electron rocket itself weighs ~7x the maximum carrying capacity of the F-104.

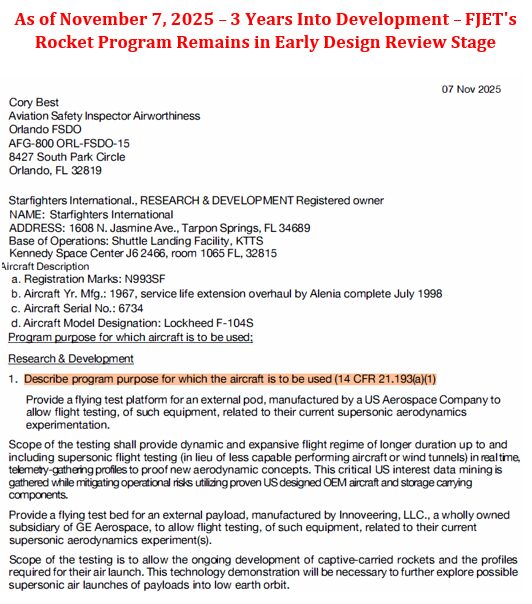

At the end of the day, evaluating FJET’s specs is an exercise in faith, not analysis. As of this writing, no rocket has been built, no motor has been test-fired, no rocket has been released from an F-104 in flight, and no powered flight of any kind has been conducted. The program remains at the design review stage after more than three years of development. The two most recent FAA program letters for jet N993SF, from December 2024 and November 2025 describe the scope of testing as “to allow the development of captive-carried rockets and the profiles required for their air launch” – language that describes a program still working toward the conditions necessary to attempt a launch, not one approaching it.

Starfighters Has Been Attempting Air-Launch for Over a Decade

FJET’s bold plan may be new to investors, but it has been attempting to launch rockets from F-104s for over a decade. The current program is the fourth iteration. Every prior attempt failed.

The first began in late 2011 as a NASA-funded collaboration between Starfighters Aerospace, 4Frontiers Corporation (a Florida-based NewSpace company), and Embry-Riddle Aeronautical University. The project, branded StarLab, aimed to air-launch a suborbital sounding rocket from an F-104. In October 2011, a motorless prototype was mounted under the wing at Kennedy Space Center for ground testing. FJET’s Svetkoff projected 100 commercial missions annually by 2013. No StarLab rocket was ever launched. The 4Frontiers partnership dissolved without a single powered flight test.

The second iteration, in 2016, was a partnership with CubeCab, a startup planning to launch 10 kg CubeSats from F-104 underwing pylons at up to 100,000 feet. CubeCab was “hoping to begin operations as early as 2018”. CubeCab never launched a single rocket. It now appears defunct, with no update on its progress after the planned launch date passed. Its COO now works as a Linux Administrator.

The third involved Italy’s National Research Council (Consiglio Nazionale delle Ricerche, or CNR) under a program called AVIOLANCIO. In November 2022, Starfighters conducted one captive-carry test – an inert, motorless prototype mounted under an F-104 wing. The program manager called it the “first test” and described a pathway toward suborbital flight. That was the last FJET ever contributed. CNR subsequently moved the avionics contract to GMV, flight testing to FTR Enterprises, and by December 2025 had switched carrier aircraft from the F-104 to a Dassault Alpha Jet entirely.

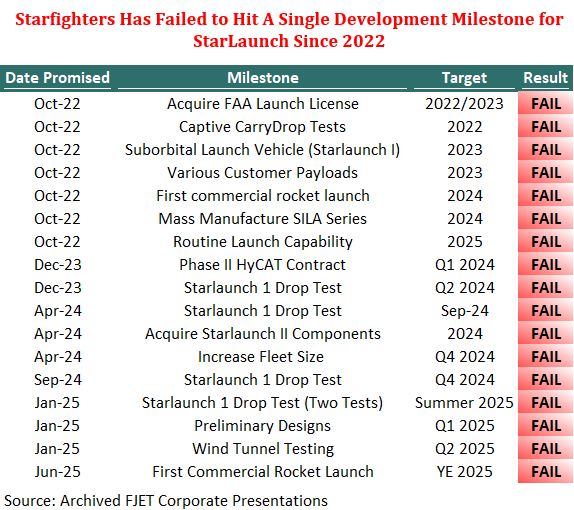

Timelining Starfighters’ Broken Promises: Every Development Milestone Has Been Missed Since 2022

FJET’s failure to hit any of its development milestones since 2022 suggests the fourth air launch iteration will follow in the footsteps of the prior three attempts.

The earliest development timeline on record is an October 2022 deck published shortly after Fortuna took over. Similar to other company’s Fortuna has been involved in FJET outlined an aggressive roadmap: captive-carry and drop tests in 2022, a suborbital vehicle and IPO by 2023, mass manufacturing and first commercial launch in 2024 and routine launch capability by 2025. The deck also stated the company was “in the process of acquiring a launch license with the FAA.”

None of it has happened. The only flight activity in 2022 was a November captive-carry of the CNR, an inert, motorless prototype with no connection to the proprietary StarLaunch program. By April 2023, the company had published a new presentation that was nearly identical to the October 2022 deck. Eight months had passed and not a single milestone had been updated.

In December 2023, FJET announced a subcontractor role under GE Aerospace’s HyCAT initiative, a hypersonic testing program with no direct connection to orbital launch. No public update on HyCAT’s progress has been provided since. That same year-end update promised hypersonic contracts in Q1 2024 and StarLaunch I drop tests by Q2.

The Q1 2024 update, published in April, quietly slipped the drop test to September and described it as “the last major physical test hurdle.” The company also promised Platform II component acquisition by Q4 2024 and fleet expansion. September passed without a drop test. Q4 passed without Platform II.

The year-end 2024 update, published January 3, 2025, made no mention of the missed drop test or the stalled F-4 deal. It described a “year of progress” and declared that “Starfighters embarks upon 2025 with a well-charted path.” Drop tests were promised again – for the third consecutive year. In March 2025, the company reported completing “the external surface (outer skin) engineering” of the StarLaunch I test article and targeted first commercial launch by year-end. The year ended with no commercial launch.

In over three years, the promises of captive-carry tests, drop tests, a suborbital vehicle, mass manufacturing, commercial launches, and routine launch capability have yielded wind tunnel testing and a design review announcement. Every milestone, every flight test, every acquisition, and every launch date has been missed.

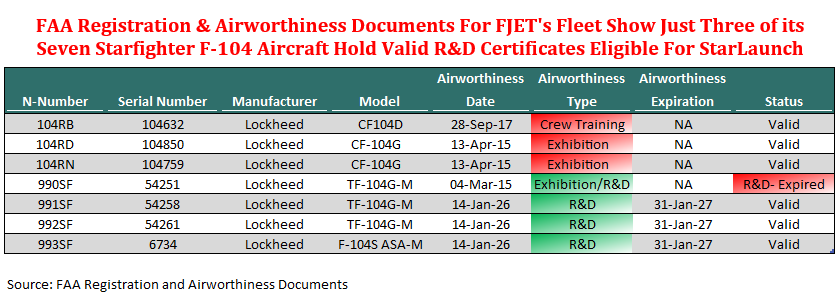

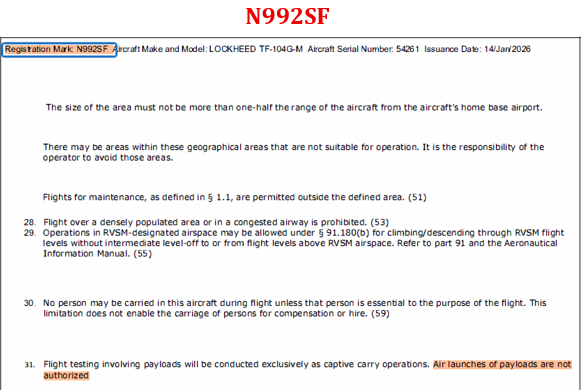

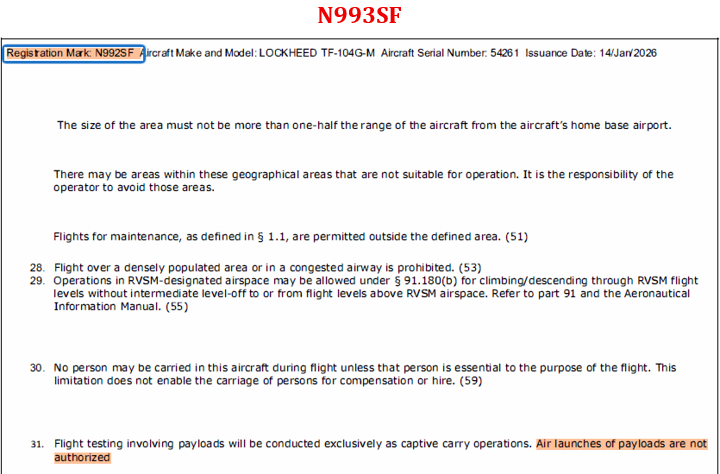

FAA Registration and Airworthiness Documents Show FJET’s Fleet Includes Just Three R&D-Certified Aircraft; FJET Could Not Confirm the Availability of Korean Aircraft Purchased for StarLaunch II

We obtained registration and airworthiness documents from the FAA for all seven F-104 Starfighters which FJET claims to have in its fleet. These are retired military aircraft — they hold no standard FAA type certificates and fly instead under Experimental Airworthiness Certificates issued under 14 CFR Part 21, which authorize flight only for specific, limited purposes.

While FJET boasts that it has a fleet of seven commercial F-104, the documents indicate that only three (N993SF, N992SF, N991SF) of the seven jets currently hold active R&D certificates eligible for the StarLaunch program. The remaining four aircraft (N104RB, N104RD, N104RN, N990SF) hold only Exhibition, Crew Training, or expired R&D certificates.

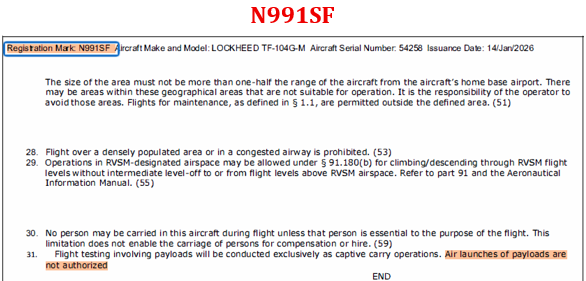

The documents also reveal that all three R&D certificates contain “Limitation #31” prohibiting their use as a launch vehicle: “Flight testing involving payloads will be conducted exclusively as captive carry operations. Air launches of payloads are not authorized.”

FJET’s granted R&D certificates have also been issued with unusually short terms. Permits can be issued for up to 3 years, however, the current certificates for all three FJET R&D jets expire after just twelve months. Separately, the company does not hold a commercial space launch license under 14 CFR Parts 415 and 431, issued by a completely different FAA office (the Office of Commercial Space Transportation).

FJET’s has also voiced ambitions for a StarLaunch II platform which depend on acquiring F-4 Phantom IIs – a significantly larger aircraft than the F-104. In 2024, the Company signed an agreement with Aerovision LLC to purchase twelve F-4s across four phases totaling $20 million, with an initial $5 million deposit, but the deal has fallen flat. By February 2025, FJET disclosed it had been unable to inspect the aircraft, could not confirm their availability, and had paid not paid the required deposits. The agreement was subsequently amended, via a verbal agreement, pushing deadlines back and allowing FJET to walk away from later phases entirely. As of September 30, 2025, FJET had made total deposits of $5.15 million to Aerovision. No F-4s have been delivered and the $5 million initial deposit appears to be in limbo.

Part 3: It’s Rocket Science, But It’s Not Rocket Science…

Rocket Science 101

Justus Parmar is an outspoken Elon Musk supporter and regularly touts his SpaceX investment. So, we figure he takes Musk’s views on rocket science seriously. Elon has said “Physics is a harsh judge” and that “If you get it wrong, the rocket will blow up.”

For physics to even be able to judge Starlaunch first FJET would need to have a rocket. We could leave our research there but to give the Company every benefit of the doubt, we consider what its launch aspirations would look like if it did have a rocket.

To put FJET’s imaginary rocket to a physics test we first must iron out some of the basics on the subject.

The Kármán Line – where space begins – is set at 80-100 km depending on the defining authority. Low Earth Orbit (LEO) begins above it, spanning ~160-2,000 km above Earth’s surface, and is by far the most populated orbital regime. As of October 2025, nearly 13,000 active satellites orbit there, ~66% of which are part of SpaceX’s Starlink constellation.

The real hurdle is not reaching LEO but achieving sufficient horizontal velocity to stay there. Orbital velocity works because the Earth’s surface curves away beneath a falling object at the same rate it falls. This means something moving fast enough sideways never actually hits the ground. Without that velocity, a vehicle arcs back to Earth.

That required velocity is captured by delta-v: the total speed change a vehicle must achieve to complete a maneuver in space. Reaching LEO requires ~9,100-9,400 m/s of delta-v – dominated by orbital velocity itself (~7.8 km/s) plus an additional 1,300–1,800 m/s lost fighting gravity and drag during ascent.

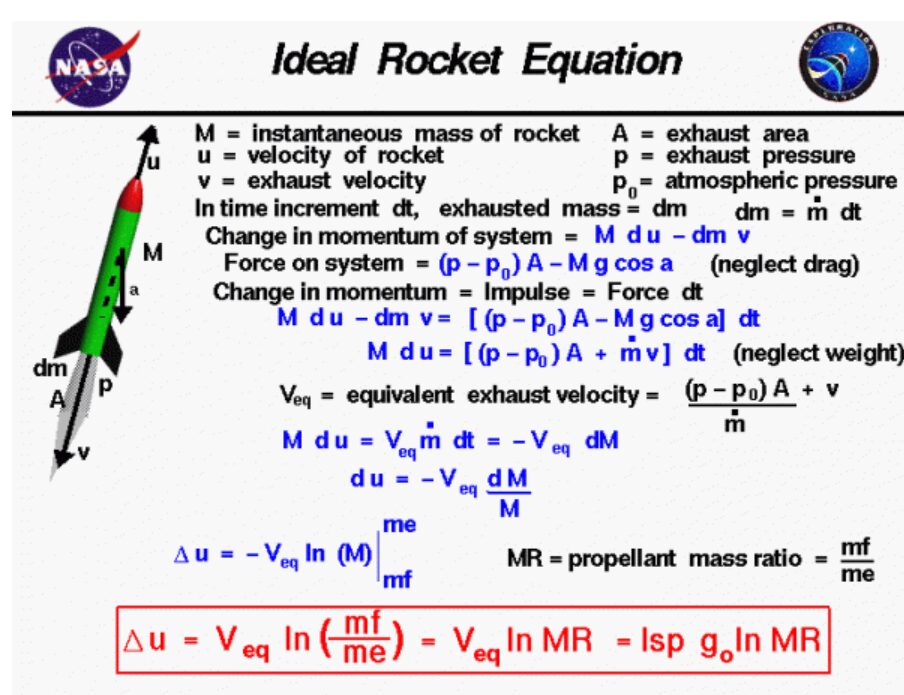

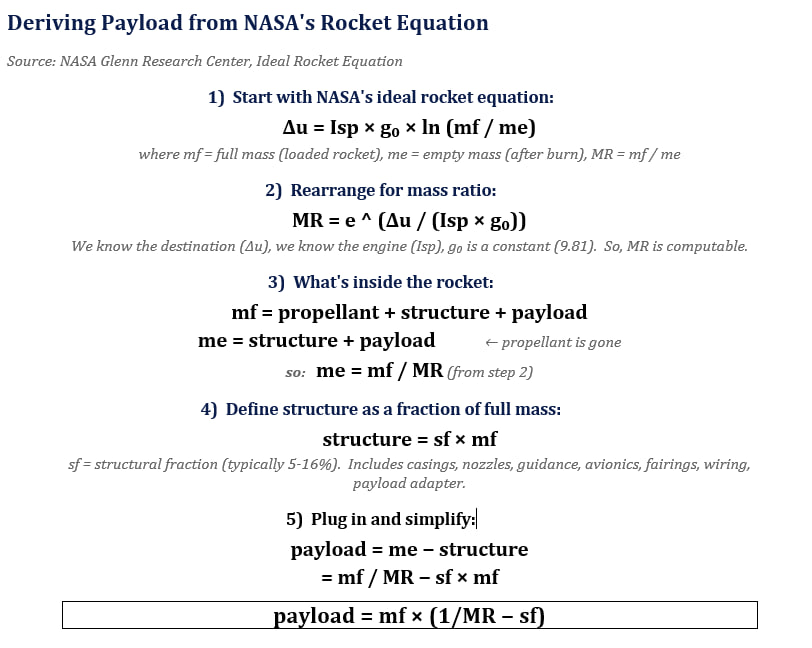

The Tsiolkovsky rocket equation (the “rocket equation”), published in 1903, governs how much fuel a rocket needs to produce a given delta-v. Its critical insight is that the relationship between delta-v and propellant mass is exponential, not linear. This is why 85-90% of the rocket’s launch weight is typically fuel and why delivering even a small payload to orbit demands an enormous amount of propellant.

The central question for FJET is whether it can launch a rocket into LEO. The Company claims it can deliver 100kg to orbit – and up to 400kg if four StarLaunch I rockets are carried simultaneously – at a cost per kg that competes with leading platforms backed by billions of dollars. These are extraordinary claims from a company that has never developed a rocket. Nevertheless, we apply the rocket equation to find out whether physics supports them.

Because we know the approximate delta-v required for a rocket to reach orbit, we can make assumptions around other variables in the equation to back into a rocket’s potential payload capacity. In our analysis, we model a blue-sky scenario where FJET develops a rocket with the best specs in the market – SpaceX-level structural efficiency and engine efficiency. However, as the analysis shows, even after giving FJET this huge benefit of the doubt, the F-104 would fail to deliver its projected payloads of 100kg to LEO.

The fundamental problem with air launch is that the mass of a rocket – a key variable in the rocket equation (mf) – that an aircraft can carry is constrained by the carrying capacity of the aircraft itself. This makes it even more remarkable that FJET promotes the F-104 as the carrier aircraft for a launch platform. The F-104 has the lowest payload capacity of all the carriers that have attempted air launch.

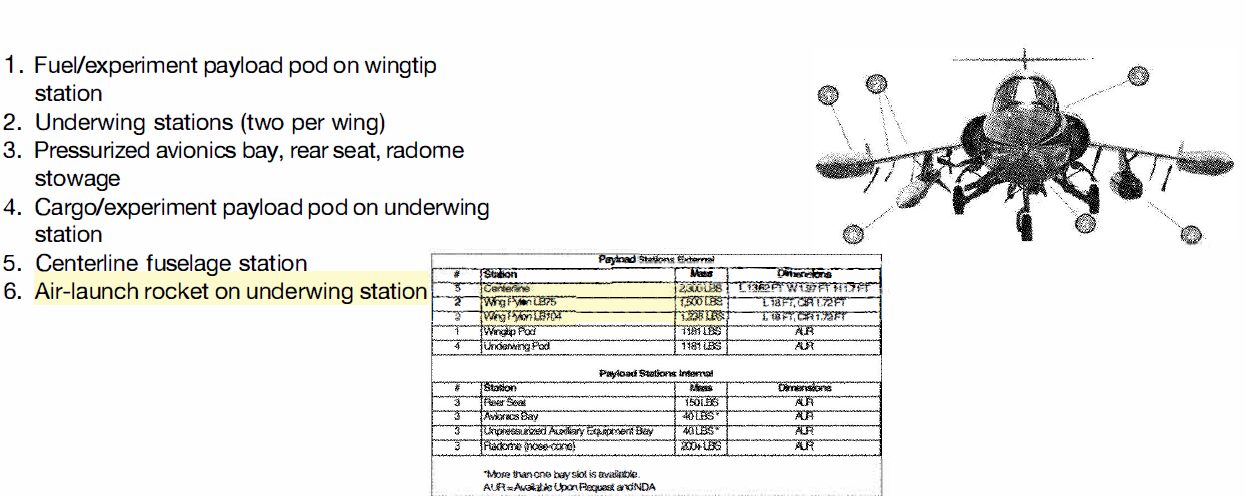

The F-104’s low payload capacity must then be distributed across the aircraft, which further constrains the mass of the rocket it can carry. Based on FAA airworthiness documents, previous tests with the Italian CNR program, and Company’s own social media, FJET’s rocket will most likely sit under the wing of the aircraft.

Airworthiness documents for all three of FJET’s R&D-certified aircraft show the same underwing configuration in a diagram, with “Station #6” labeled “Air-launch rocket on underwing station.” Depending on the attachment – referred to as a pylon – the underwing configuration supports rockets of up to 1,500 lbs (680 kg).

Alternatively, FJET could also use the F-104’s centerline fuselage station (under the plane) to carry a rocket. The Company has not indicated any plans for this, but NASA has done it in the past. In this configuration FJET could carry a rocket weighing up to 2,300 lbs (1,043 kg).

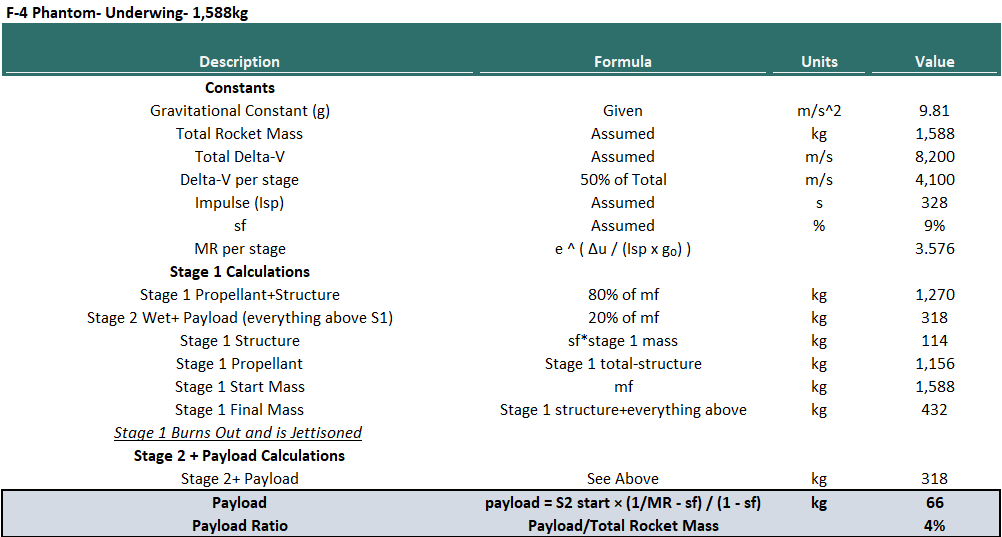

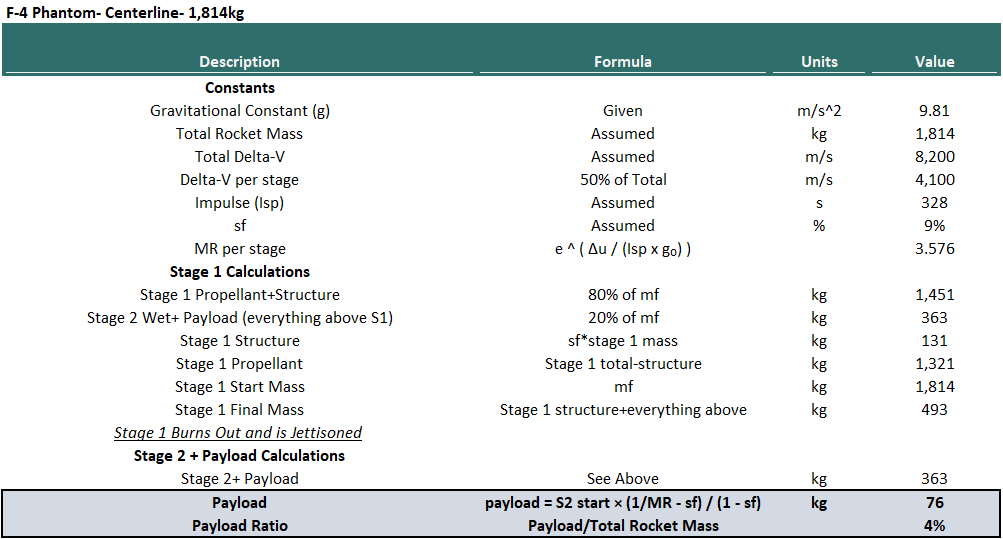

Still, a third option available to FJET would be to upgrade its carrier aircraft to the F-4 Phantom which it has attempted to acquire unsuccessfully. While FJET has yet to even confirm the existence of the F-4 aircraft in Korea, we give them the benefit of the doubt and model this alternative. The F-4 can carry up to 18,650 lbs (8,460 kg). Our F-4 analysis uses the most generous station-level figures available – 3,500 lbs (1,588kg) per underwing station and 4,000 lbs (1,814kg) for the centerline fuselage station.

“Physics is a Harsh Judge”

After rearranging the rocket equation to solve for payload capacity we are left with payload = mf x (1/MR – sf). The steps to derive this formula are shown.

The Mass Ratio (MR) tells us how much of a rocket must be propellant versus structure, engines, and payload. It is calculated as: MR = e ^ (Δu / (Isp x g₀)), using three inputs:

g₀ – gravitational acceleration: 9.81 m/s². A constant.

Δu (delta-v) – F-104 contributes 650 m/s of delta-v before releasing the rocket. This analysis uses 8,200 m/s as the delta-v the rocket must produce on its own thereafter. The same delta-v assumption is used for the F-4 Phantom scenarios, as both aircraft operate at similar speeds and altitudes.

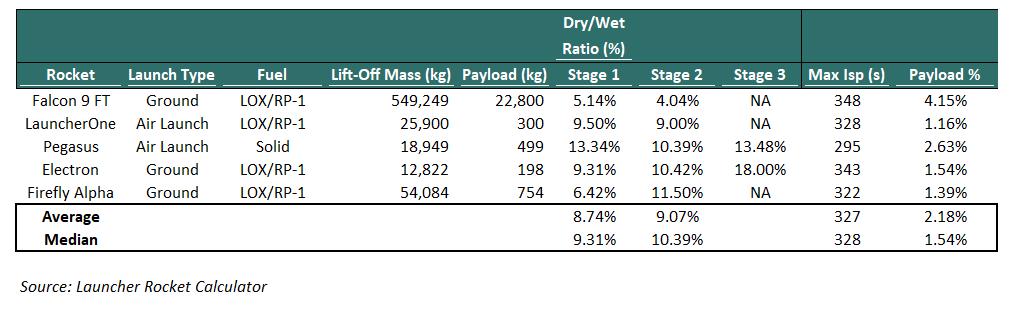

Isp (specific impulse) – a measure of engine efficiency, expressed in seconds (s). The higher Isp means more thrust per kg of propellant burned. It is determined by the propellant type and engine design, neither of which FJET has disclosed. We make an assumption for Isp that benchmarks against five operational rockets using the open-source Launcher Rocket Calculator, developed by Launcher. Isp varies by propellant type – solid propellant typically delivers 265-295s, liquid LOX/RP-1 engines 290-348s – and by whether the engine is optimized for sea-level or vacuum operation. Once again FJET has disclosed nothing about its propulsion system, however, we take each benchmarked rocket’s maximum stage Isp and use the median of the five vehicles for our analysis.

The Isps in the benchmark group range from 295s (Pegasus, solid propellant) to 348s (Falcon 9, LOX/RP-1 vacuum-optimized), with a median of 328s. The median Isp is swayed by higher Isp due to the prevalence of liquid propellant. Solid propellant – more common for small air-launch rockets – would yield 270-295s and materially worse results. The assumed 328s effectively grants FJET world-class, liquid-engine performance to FJET which has never built, tested, or fired a rocket engine of any kind.

With g₀, delta-v, and Isp, the mass ratio (MR) can be derived. The remaining variables of the rocket equation are then mf (full rocket mass) and sf (structural fraction).

mf (full rocket mass) is the total mass of the rocket at ignition: propellant, structure, and payload combined. This is the one variable known with certainty because it is constrained by the aircraft’s pylon capacity. We ran the analysis across the previously mentioned four configurations across FJET’s two potential aircraft carriers.

sf (structural fraction) is the percentage of the rocket’s total mass, excluding rocket propellant and payload. It accounts for weight from things such as guidance systems and internal rocket structures. The higher the structural fraction, the less mass available for payload. FJET does not provide these metrics either. So, again, we use benchmarks from the Launcher Rocket Calculator, specifically each rocket’s dry-to-wet mass ratio – a stage’s structural mass divided by its total mass, including propellant and excluding payload. The peers and their respective stats are shown in the table above.

From the data we can observe that structural efficiency deteriorates as rockets get smaller. This is due to components with minimum, fixed masses that do get smaller as the rocket does. We can also infer that air launch vehicles carry additional structural requirements that ground-launched vehicles do not.

We use a structural fraction of 9%, representing the approximate stage 1 median across the five benchmarked vehicles. NASA cites a “rule of thumb” that approximately 90% of an orbital rocket’s mass is propellant, leaving roughly 10% for everything else. Internal rocket structures make up the majority of the remaining 10%

Most rockets use something called “staging”, which splits the vehicle into sections that fire sequentially. When a lower stage burns out, it is separated from the upper stage, which delivers improved mass efficiency at each individual stage and, as a result, a lower delta-v. FJET has positioned StarLaunch as a ‘multistage’ rocket system but has not disclosed the number of stages or specs between them. This analysis assumes a two-stage design, consistent with other benchmarked rockets.

The following table shows the distribution of mass and delta-v across stages for the five benchmarked rockets. For three-stage rockets – Pegasus and Electron – the upper stages are combined into a single “Stage 2” figure for comparability.

The data shows a consistent pattern. Stage 1 accounts for ~80% of total rocket mass across every vehicle in the table. The upper stage(s) account for ~20%. The distribution is explained by Stage 1 having to lift the entire rocket and payload while fighting full gravity and punching through the densest layers of the atmosphere. Stage 2 consistently contributes more delta-v than Stage 1 because Stage 1 engines are made less efficient by the thick lower atmosphere, whereas Stage 2 operates in near-vacuum conditions.

This analysis applies a uniform Isp of 328s and a uniform structural fraction of 9% across both stages. When the engine efficiency and structural fraction are the same, the delta-v contribution by each stage is split evenly.

The assumptions derived from this full exercise are now ready to be used to compute the payload capacity of FJET’s F-104 and F-4 (that they can’t find in Korea). The results are as follows.

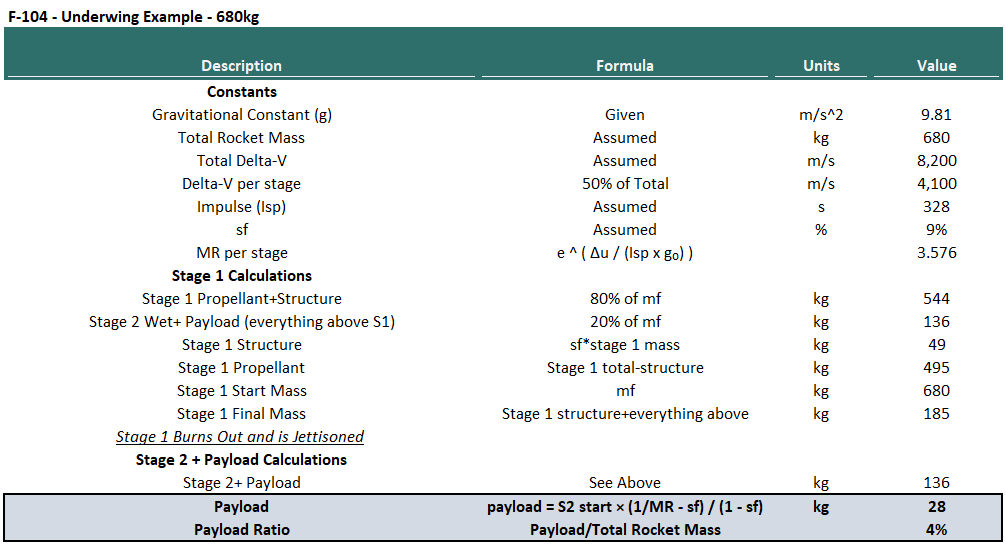

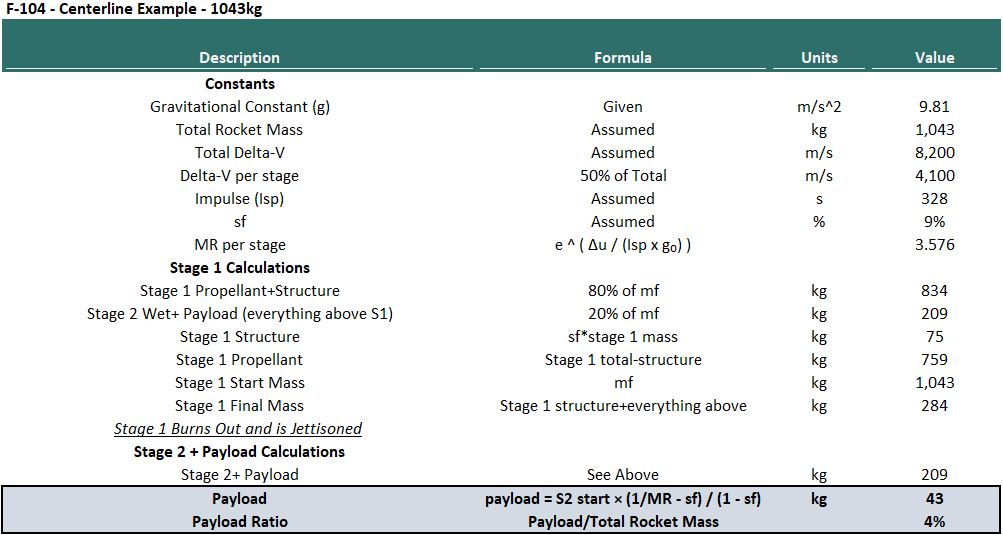

FJET’s website claims a single Starlaunch rocket carried on an F-104 has a payload capacity of 100 kg to LEO. That figure was pulled out of thin air. In our analysis – which is grounded in the rocket equation – the base-case result for the F-104 underwing is 28 kg, or 72% lower than FJET”s claim. Even on the F-104 centerline configuration, which is not contemplated in any of FJET’s materials, it would still carry just 42 kg.

The F-4 Phantom scenarios still fall short. The underwing configuration delivers 64 kg, and the centerline delivers 73 kg. The results from a plane that FJET has not even confirmed is available to them still fall well short of the 100 kg claim.

Across all four configurations we ran through the rocket equation, the maximum payload to LEO is approximately 4% of total rocket mass which is after making extraordinarily generous assumptions for FJET. It matches SpaceX’s Falcon 9, the most mass-efficient orbital rocket ever built, at 4.15%. Real-world payload fractions for small rockets and air-launched vehicles are materially lower: Pegasus achieves 2.63%, Electron 1.54%, and LauncherOne 1.16%.

Part 4: Three Decades of Air Launch Failure

Frankly, running assumptions about FJET’s imaginary rocket through a physics equation probably was not necessary to prove our point. An easier way to understand FJET’s probability of success is to look at the graveyard of well-capitalized air launch platforms that preceded it.

As the previous section showed, almost every air-launch-to-orbit system ever attempted has used a carrier with significantly greater payload capacity than the F-104 and each has ended in failure, bankruptcy, or abandonment. Even Pegasus – the lone orbital success – was rendered obsolete by competition from SpaceX, flying just three niche government missions since 2016.

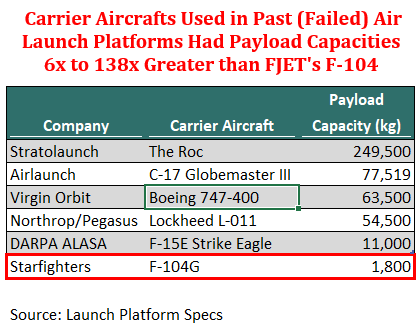

Pegasus used a Lockheed L-1011 TriStar rated to 51,000 lbs. Virgin Orbit used a Boeing 747-400 and burned through $1 billion before filing for bankruptcy. Stratolaunch built the world’s largest airplane at 550,000 lbs capacity and abandoned orbital launch entirely. DARPA spent $164 million with Boeing mounting a rocket on an F-15E Strike Eagle rated to 24,500 lbs and canceled the program after two propellant explosions. AirLaunch LLC used a C-17 Globemaster III, successfully test-dropping 65,000 lbs and ran out of funding. Generation Orbit received an X-plane designation from the Air Force and never flew.

If none of these platforms succeeded, the F-104 Starfighter which has a fraction of their carrying capacity and no demonstrated rocket offers no credible solution.

Pegasus: Lone Success, Now Obsolete

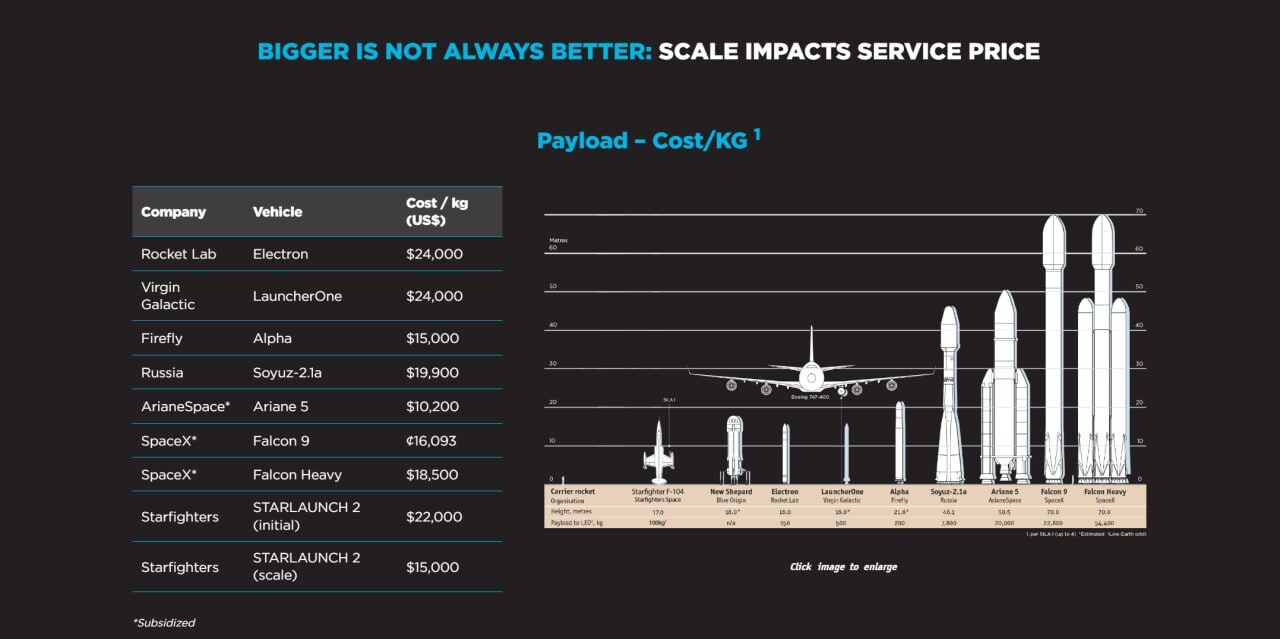

Pegasus, developed by Orbital Sciences (now Northrop Grumman), was the world’s first privately developed orbital launch vehicle, flying for the first time in 1990. Over 31 years and 45 missions it launched nearly 100 satellites with an 89% success rate, the only air-launch-to-orbit system in history to achieve sustained operation. Its carrier, “Stargazer,” is a modified Lockheed L-1011 TriStar wide-body airliner capable of carrying 51,000 lbs to 42,000 feet.

Pegasus XL, the latest variant, is a three-stage solid-propellant rocket purpose-built for air launch, including a delta-shaped wing on its first stage to manage the aerodynamic forces of release at altitude. Its first stage produces approximately 726 kN (163,247 lbf) of thrust — roughly four times the 41,000 lbf total thrust FJET claims for Starlaunch I across all stages combined. Weighing 23,100 kg at launch, or roughly 22 times the F-104’s maximum payload capacity, it can deliver 443 kg to LEO.

Pegasus was rendered economically obsolete by reusable ground-launched rockets. By 2008, NASA was its sole customer, and even that relationship eroded. In 2019, Northrop lost the IXPE launch contract to SpaceX despite IXPE having been specifically designed for Pegasus’ payload fairing. The Falcon 9, capable of carrying 50 times the payload mass to LEO was simply cheaper. Since 2016, Pegasus has flown just three niche government missions that SpaceX rideshare couldn’t serve for orbital geometry reasons. In 2025, Northrop drew down on its last Pegasus XL in inventory.

At $63,000–$126,000 per kg – 3-6x the cost of a Falcon 9 launch – the only successful air-launch system ever, backed by a wide-body airliner, a purpose-built three-stage rocket, and the full resources of Northrop Grumman, could not compete on price. Now FJET proposes to surpass it carrying less than 5% of the rocket mass and no demonstrated propulsion system.

Virgin Orbit: A Space Virgin Forever

Virgin Orbit (“Virgin”) was spun out of Virgin Galactic in 2017 by Sir Richard Branson. The company went public in August 2021 via a SPAC merger, raising $228 million – less than half its targeted $483 million raise due to significant shareholder redemptions.

LauncherOne, Virgin’s two-stage air-launched liquid-propellant rocket, was designed to deliver up to 300 to 500 kg to LEO depending on orbital inclination. Its first stage produced 327 kN (73,500 lbf) of thrust and weighed approximately 26,000 kg at launch – roughly 25 times the F-104’s maximum payload capacity. Virgin’s carrier, “Cosmic Girl,” was a modified Boeing 747-400, capable of carrying LauncherOne to 35,000 feet before release.

Virgin reached orbit four times on six attempts between 2020 and 2023, deploying 33 satellites for customers including NASA, the US Department of Defense, and the Royal Netherlands Air Force. Virgin experienced technical issues, including a broken high-pressure liquid oxygen feed line which saw its rocket fall into the Pacific on its first mission, as well as a dislodged fuel filter which led to nine customer satellites being lost on its final mission.

In Q3 2022, Virgin lost $44 million against $31 million in revenue, cutting its launch projection for 2022 from 12 to 4-6 launches. The company filed for Chapter 11 bankruptcy on April 4, 2023. Its assets – HQ, factory, carrier aircraft, and test site – sold at auction for approximately $36 million total. A company backed by Richard Branson that held a $4B valuation upon coming public still could not build a sustainable business. SpaceX rideshare at $6,000 per kg rendered their alternative uneconomical.

Stratolaunch: World’s Largest Aircraft Carrier Abandoned Orbital Launch

Stratolaunch Systems was founded in December 2011 by Microsoft co-founder Paul Allen and Scaled Composites founder Burt Ruta, the same team behind SpaceShipOne, which won the $10 million Ansari X Prize in 2004. Stratolaunch was slated to begin flights in 2015 and have its first orbital launch in 2016.

The company’s carrier aircraft, the “Roc”, is the world’s largest aircraft by wingspan at 385 feet. It has a payload capacity of 550,000 lbs and was designed to carry up to three Pegasus XL rockets simultaneously.

Stratolaunch spent years cycling through launch vehicle partners. It worked with SpaceX, Orbital Sciences, then a proprietary design before settling on Pegasus XL in 2016. At its most ambitious, the Roc was projected to loft 6,100 kg to LEO before SpaceX walked away within a year.

The company never launched a single rocket into orbit. Paul Allen passed away in October 2018. Months later, Stratolaunch abandoned its proprietary launch vehicle family entirely. The Roc completed its maiden test flight April 2019 reaching 17,000 feet – then Stratolaunch’s owner put the entire company up for sale at $400M. It was acquired by Cerberus Capital Management, which pivoted the company away from orbital launch into hypersonic test flights for the government. The company is now focused on developing the Talon-A rocket with the government. The world’s largest aircraft, built specifically for orbital air launch, never launched anything.

DARPA/ALASA: Starfighters’ Most Direct Parallel

In November 2011, the US Defense Advanced Research Projects Agency (DARPA) – the US Department of Defense’s central R&D organization – launched its Airborne Launch Assist Space Program (ALASA), aimed at launching 45 kg satellites to LEO for under $1 million per flight on as little as 24 hours notice. After a Phase 1 competition involving Lockheed Martin, Virgin Galactic, and Boeing, DARPA awarded Boeing a Phase 2 contract worth up to $104 million in March 2014.

Boeing’s design called for a 5,000 lb expendable rocket mounted beneath an unmodified F-15E Strike Eagle, a fighter jet capable of carrying 24,500 lbs externally, more than ten times the F-104’s maximum payload capacity. The jet would climb to 40,000 feet, release the rocket, and return to base as a reusable first stage. The concept is identical to what FJET is marketing to investors today.

The program never launched. Boeing tested its novel monopropellant twice at its Promontory, Utah facility. Both times it exploded. DARPA’s program director described the propellant as “finicky” and concluded it was too dangerous to store aboard a piloted aircraft. In November 2015, DARPA cancelled all planned flight tests.

The total DARPA planned budget was ~$164M, had Boeing as prime contractor, and used a fighter jet with more than ten times the F-104’s carrying capacity. Targeting just 45 kg to orbit, they could not make it work.

Air Launch & Generation Orbit: The List Goes On…

AirLaunch LLC, selected by DARPA in 2003 for its Falcon Small Launch Vehicle (SLV) program, developed QuickReach, a two-stage liquid-fueled rocket designed to be gravity-dropped from the cargo bay of a C-17 Globemaster III. It aimed to be able to launch 1,000 lbs to LEO on 24 hours notice for under $5 million per flight. The company completed successful drop tests of a 65,000 lb inert booster at 29,500 feet and advanced through Critical Design Review before the program concluded in 2008. DARPA and the Air Force collectively invested $38 million. AirLaunch was put into hiatus and never launched.

Generation Orbit, founded in 2011, won a NASA contract and earned an official X-plane designation from the Air Force for its X-60A hypersonic vehicle. Its first flight, planned for late 2019, was delayed indefinitely. No further updates have appeared since 2020. SpaceWorks’ own website now lists X-60A under “Past Projects.”

Combined, these programs consumed hundreds of millions in capital and produced exactly one commercially operational air-launch system (now down to its last rocket). FJET’s proposes to succeed with an F-104 Starfighter where a Boeing 747, an L-1011 TriStar, the world’s largest airplane, an F-15E Strike Eagle, and a C-17 Globemaster III have all failed.

Conclusion

FJET is not a rocket launch company. It is a stock promotion.

In over three years under Fortuna’s stewardship, it has spent almost nothing on R&D, missed every milestone it has ever communicated to investors, and relied on stock imagery renderings in its materials. It is no wonder its founder, Rick Svetkoff resigned two months after the IPO. The FAA has explicitly stated that air launches from its fleet are not authorized. There is no licensed vehicle, no tested rocket, no employees, and no credible path to orbit.

The physics are equally unforgiving. Air launch has claimed Virgin Orbit, Stratolaunch, DARPA, and Boeing. The only orbital success in three decades required a rocket 22 times heavier than anything FJET’s F-104 can carry – and SpaceX has since rendered even that obsolete. Our analysis using the Tsiolkovsky rocket equation, built on assumptions generous enough to embarrass us, suggests FJET could deliver a 72% lower payload capacity than claimed.

History doesn’t repeat but it often rhymes. Justus Parmar and Fortuna’s playbook is well-documented in this report: find a hot theme, issue cheap equity to insiders, install a recycled team, pitch an aggressive story, and pay for promotion to attract liquidity from retail investors.

The promotional infrastructure is already in place at FJET. The warrants have already been issued. The affiliates are already installed.

We are short.